Image Source: rbtcpas.com

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, does not just tweak the tax code—it restructures the economics of owning, holding, and transferring high-value real estate in the United States. For affluent buyers, existing owners, and real estate investors operating in the $3M–$10M+ price band, the changes are specific and material.

This article breaks down exactly what OBBBA means for your purchase structures, cash flow, estate planning, and location strategy.

Key Takeaways

OBBBA changes the after-tax math for luxury real estate.

Bonus depreciation can improve year-one investor cash flow.

The higher estate exemption supports long-term wealth transfers.

Opportunity Zones strengthen Puerto Rico’s luxury investment appeal.

Proper structuring is critical before buying or selling.

How OBBBA Changes the Luxury Real Estate Math

Before OBBBA, high-net-worth buyers factored in depreciation phase-downs, uncertain QBI treatment, and a looming estate tax cliff when modeling the true cost of a luxury acquisition. OBBBA removes most of that uncertainty by making several key provisions permanent. The result is a measurable reduction in the after-tax cost of ownership for properties held in the right structure.

Consider a $7M residential investment property held through an LLC. With 100% bonus depreciation reinstated, the owner can expense a significant portion of the depreciable basis in year one, generating a substantial paper loss that offsets other income. Pair that with the permanent 20% QBI deduction on net rental income, and the effective tax rate on that property's cash flow drops considerably compared to pre-OBBBA projections.

Personal Tax Rates and SALT Cap Changes

OBBBA makes the Tax Cuts and Jobs Act's (TCJA) individual rate structure permanent, which matters for buyers who hold luxury properties in their own name rather than through an entity. The top marginal rate stays at 37%, and the expanded standard deduction remains in place. For luxury homeowners who itemize, the SALT cap increase is the more relevant change.

The SALT deduction cap temporarily rises to $40,000, up from the previous $10,000 limit, for eligible itemizers.

The benefit phases down at higher income levels, reducing the value of the increased cap for top‑earning households; exact thresholds vary by filing status and will be refined through IRS guidance.

The mortgage interest deduction retains the $750,000 acquisition debt limit—no change here for buyers financing luxury purchases.

Itemized deduction limits for the top bracket remain in place, so the SALT increase does not translate into a dollar-for-dollar increase for all high earners.

For a buyer purchasing a $4M primary residence in a high-tax state like New York or California, the SALT increase from $10,000 to $40,000 represents real money—potentially $30,000 in additional deductible state and local taxes annually. That is not a minor footnote. It changes the annual carrying cost calculation in a way that makes high-tax-state luxury ownership more competitive than it has been since 2017.

Bonus Depreciation and After-Tax Cash Flow

Perhaps the single most impactful change for real estate investors under OBBBA is the permanent reinstatement of 100% bonus depreciation on qualifying property. This applies to personal property components within a luxury real estate acquisition—think furniture packages, appliances, fixtures, and certain land improvements. For a $5M luxury rental property, a cost segregation study might identify $800,000–$1.2M in personal property eligible for immediate expensing.

Year-one depreciation deductions can dramatically reduce or eliminate taxable rental income.

Losses generated may offset other passive income streams, depending on the investor's classification.

Real estate professionals (as defined by the IRS) can use these losses against active income—a significant advantage for full-time investors.

The reinstatement applies to qualified property acquired and placed in service after January 19, 2025, and transitional rules allow elective expensing in the first taxable year ending after that date.

This is not a new concept, but the permanence matters. Investors can now underwrite deals with full bonus depreciation baked in without worrying about phase-downs disrupting their projections in years two through five.

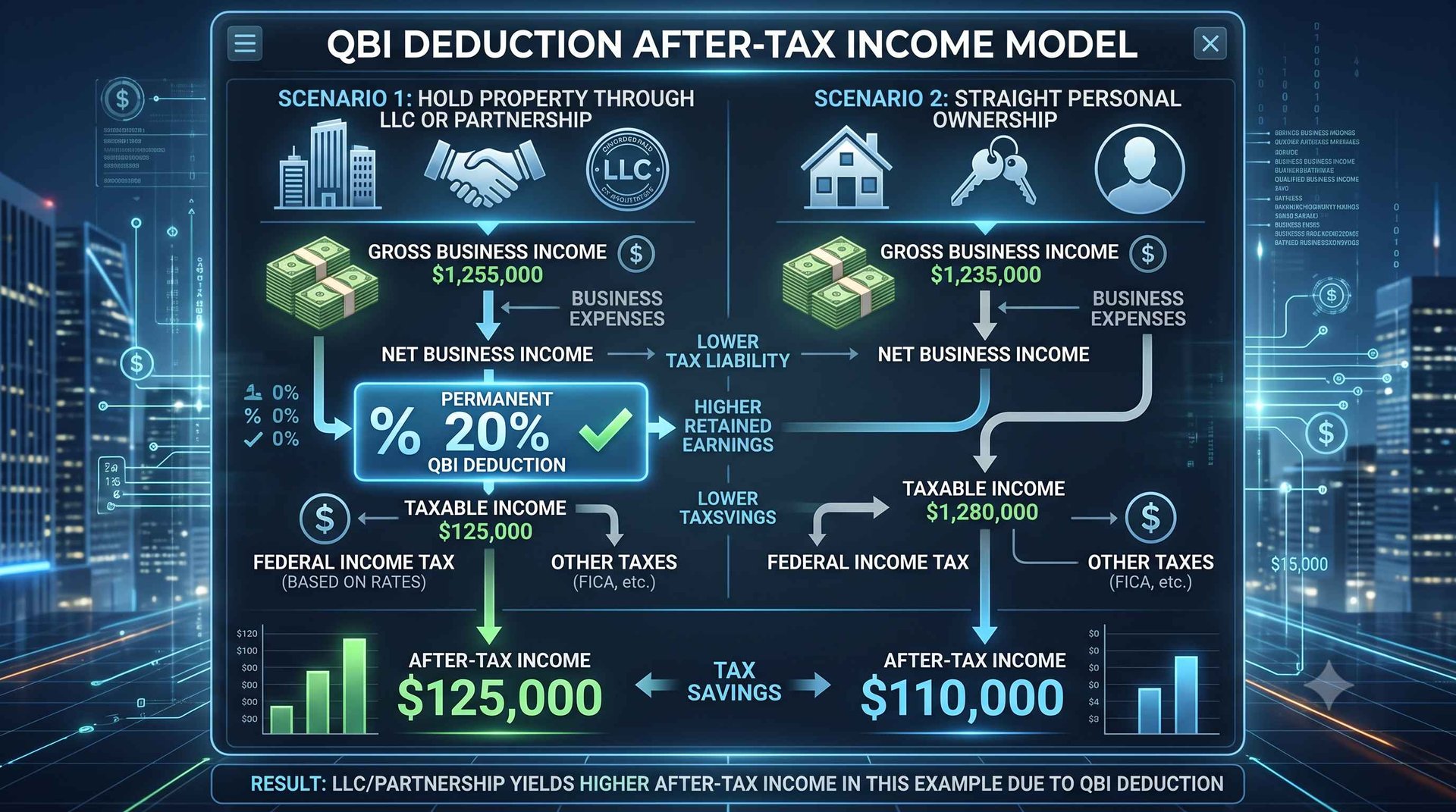

QBI Deduction and Pass-Through Structures for Luxury Properties

The permanent extension of the 20% Qualified Business Income (QBI) deduction is a significant win for investors who hold luxury properties through pass-through entities. LLCs, partnerships, S corporations, and REIT investors all benefit from this provision, which effectively reduces the top federal rate on qualifying real estate income from 37% to approximately 29.6%. That is a structural advantage that compounds over time on high-value assets.

For REIT investors specifically, OBBBA confirms that REIT dividends continue to qualify for the 20% QBI deduction—an important consideration for high-net-worth individuals who hold luxury real estate exposure through publicly traded or private REIT structures alongside direct property ownership.

Structuring Luxury Purchases Under OBBBA

The choice between personal ownership and entity ownership for a luxury property has always involved trade-offs. OBBBA shifts that calculus in favor of pass-through entities for investment-oriented acquisitions. Here is how to think through the decision:

Identify the property's primary purpose. Is this a primary residence, a short-term rental, a long-term investment, or a mixed-use asset? The answer determines which OBBBA provisions apply most directly.

Run a cost segregation analysis. For any property above $2M, a cost segregation study will quantify the bonus depreciation opportunity and inform whether entity structuring makes sense.

Model the QBI deduction. If you hold the property through an LLC or partnership, calculate the after-tax income under the permanent 20% QBI deduction versus straight personal ownership.

Factor in estate planning. With the estate and gift tax exclusion now at $15M per individual, holding high-value real estate in a structure that facilitates gifting or trust transfers becomes more attractive.

Consult a tax advisor before closing. The interaction between bonus depreciation, QBI, and passive activity rules is complex. The structure you choose at acquisition is difficult to change later without triggering tax consequences.

Estate and Gift Tax Exemption: What $15M Means for Luxury Real Estate Transfers

OBBBA permanently sets the unified estate and gift tax exclusion at a high, inflation‑indexed level—currently approximately $15 million per individual and $30 million per married couple, with the exact dollar amounts adjusted over time. For high-net-worth families who hold significant real estate wealth, this is the provision that reshapes multi-generational planning most directly. A couple owning a $12M beachfront estate, a $6M city penthouse, and a $4M vacation property now has room to transfer all of it without triggering federal estate tax—assuming proper planning.

The inflation indexing is not a small detail. It means the exclusion grows over time, preserving its real value and giving families a longer runway for structured transfers through trusts, family limited partnerships, or direct gifting programs.

Practical Implications for Luxury Real Estate Estate Planning

Families with combined real estate portfolios under $30M can now transfer assets to heirs with zero federal estate tax exposure.

Irrevocable trusts, Grantor Retained Annuity Trusts (GRATs), and Qualified Personal Residence Trusts (QPRTs) remain useful tools, but the urgency to act before a sunset has been removed.

The higher exclusion makes outright gifting of appreciated luxury properties more viable without the pressure of a tax cliff deadline.

International buyers with U.S. luxury properties should note that non-resident alien estate tax rules differ significantly—the $15M exclusion does not automatically apply to foreign nationals.

The estate and gift tax exemption high net worth families benefit from under OBBBA pairs well with Puerto Rico's Act 60 incentives for residents who have relocated to the island.

Opportunity Zones: A Renewed Case for Targeted Luxury Investment

OBBBA makes the Opportunity Zone program a permanent feature of the tax code, with new designations scheduled every ten years and updated rules for deferral, reduction, and potential elimination of tax on qualifying gains. The extension gives investors more time to deploy capital into Qualified Opportunity Funds (QOFs) and benefit from deferred and potentially reduced capital gains treatment. For someone selling a high‑value primary residence or investment property with significant embedded gains, the Opportunity Zone pathway deserves serious attention.

Under OBBBA, gains reinvested into a Qualified Opportunity Fund can be deferred, and QOF interests held for at least ten years may elect a basis step‑up to fair market value on exit, effectively eliminating federal tax on post‑investment appreciation, subject to long‑term caps.

For a luxury real estate investor with $5M in capital gains from a prior sale, that is a meaningful deferral and potential elimination of a substantial tax liability.

Key Opportunity Zone Considerations for Luxury Investors

The 180-day reinvestment window from the date of sale still applies—timing matters.

Not all Opportunity Zone markets offer luxury-grade assets, but select markets—including parts of Puerto Rico—do.

Puerto Rico has a significant number of designated Opportunity Zones, and Puerto Rico luxury real estate in those zones can qualify for both QOF treatment and existing Act 60 tax incentives.

The combination of federal Opportunity Zone benefits and Puerto Rico's territorial tax advantages creates a layered incentive structure that few other U.S. markets can match.

Investors should work with advisors who understand both federal QOF rules and Puerto Rico's local regulatory environment to structure these transactions correctly.

OBBBA Impact by Property Type and Price Band

Not every OBBBA provision applies equally across property types and price points. The table below summarizes the most relevant changes for luxury buyers and investors across common acquisition scenarios.

The table above is a starting point, not a final answer. Every situation involves individual income levels, existing portfolio composition, and state-specific rules that interact with the federal changes OBBBA introduces.

Which Markets Benefit Most From OBBBA?

OBBBA does not treat all markets equally in practice, even if the law applies uniformly on paper. The markets that benefit most are those where the combination of OBBBA provisions and local tax environments creates the largest spread between gross and net returns. High-tax states like New York, California, and New Jersey benefit from the SALT cap increase, but they still carry high state income and property tax burdens that OBBBA only partially offsets.

Puerto Rico occupies a different category entirely:

As a U.S. territory, Puerto Rico offers federal tax benefits—including Opportunity Zone designations and OBBBA provisions—alongside its Act 60 incentive regime, which can reduce tax on Puerto Rico‑source dividends, interest, capital gains, and qualified business income to 0% for grandfathered decrees or around 4% for newer participants, subject to updated rules and residency requirements.

For high-net-worth buyers considering a U.S. luxury property investment strategy, Puerto Rico luxury real estate represents a convergence of federal and territorial incentives that no mainland market can replicate.

Why Puerto Rico Stands Out Under OBBBA

Puerto Rico luxury homes in designated Opportunity Zones can qualify for federal Qualified Opportunity Fund treatment while eligible owners benefit from Act 60 incentives on Puerto Rico‑source income, creating layered tax advantages.

Bona fide Puerto Rico residents with Act 60 decrees can secure preferential Puerto Rico tax treatment on Puerto Rico‑source dividends, interest, and capital gains:

0% for grandfathered decrees and around 4% for newer decrees—and,

under IRC section 933, Puerto Rico‑source income may be excluded from U.S. federal income tax.

Non‑Puerto Rico‑source gains can still be subject to U.S. federal tax, so careful sourcing and planning remain essential.

The OBBBA bonus depreciation rules apply to qualifying property used in Puerto Rico investment real estate, allowing accelerated expensing of eligible components and enhancing year‑one cash flow for rental acquisitions.

Qualified business income deduction rules can apply to eligible pass‑through entities holding Puerto Rico rental property, but investors should confirm how section 199A interacts with territorial sourcing and Act 60 decrees with a U.S. and Puerto Rico tax advisor, as the combined effect can materially change the effective rate.

Puerto Rico luxury real estate in markets like Dorado Beach, Condado, and Palmas del Mar has seen strong demand from relocating high-net-worth buyers, with average sales prices reflecting the quality of inventory available.

Timing Considerations for Buyers and Sellers

OBBBA creates both urgency and patience in different parts of the market. The SALT cap increase is temporary—it phases down and eventually reverts unless Congress acts again. Buyers in high-tax states who plan to hold a primary residence for five or more years should model the benefit over the window it exists, not assume it will last indefinitely. On the other hand, the permanent provisions—bonus depreciation, QBI deduction, estate tax exclusion—reward buyers who act now and hold long.

Buyers considering a primary residence in a high-tax state should move during the SALT cap window to maximize the deduction benefit.

Investors structuring luxury rental acquisitions should prioritize cost segregation studies at closing to capture full year-one bonus depreciation.

Sellers with large embedded gains should evaluate Opportunity Zone reinvestment before closing, not after—the 180-day clock starts at sale.

Estate planning reviews should happen now, even with the permanent exclusion in place, because the interaction between OBBBA and existing trust structures may need updating.

Puerto Rico Luxury Properties for Rent

For buyers and investors looking to act on the OBBBA advantages outlined above, Christie's International Real Estate Puerto Rico offers direct access to some of the island's most exclusive listings—including luxury properties for rent and for sale across Dorado, Humacao, Guaynabo, and Culebra. Whether you are exploring a primary residence under Act 60 or an investment property with Opportunity Zone potential, Christie's International Real Estate Puerto Rico connects you with the right properties and the right advisors. Real estate investment impacts.

276 Dorado Beach East, Dorado, PR 00646

This property sits within the prestigious Dorado Beach East community, one of Puerto Rico's most sought-after addresses for high-net-worth buyers seeking privacy and resort-level amenities. Its location within a designated area positions it well for buyers exploring both Act 60 residency and OBBBA-driven investment structuring.

13-14 PORT ROAD HUMACAO PR, 00791

13 & 14 Port Road is a rare Palmas del Mar luxury estate with 7 bedrooms, 8 bathrooms, 8,682 sq. ft. of living space, resort-style outdoor amenities, smart-home technology, solar power, and two buildable parcels across 1.10 acres.

A Street, Villa Caparra #A-13, Guaynabo, PR 00966

Located in the established Villa Caparra neighborhood of Guaynabo, this property offers proximity to San Juan's financial and commercial districts while maintaining a residential character that appeals to relocating executives and Act 60 applicants. It represents a practical entry point for buyers prioritizing accessibility alongside tax-advantaged residency.

11 Barrio Frailes, Culebra, PR 00775

This Culebra listing places buyers on one of Puerto Rico's most pristine outer islands, known for its protected beaches and limited development—factors that support long-term property value. For investors focused on the luxury properties for rent market, Culebra's exclusivity and natural setting generate consistent demand from discerning travelers.

Final Thoughts

OBBBA changes how high-net-worth buyers, investors, and families should evaluate luxury real estate ownership. From bonus depreciation and QBI treatment to estate planning and Puerto Rico opportunities, the strongest benefits come from proper structure before acquisition. With the right advisors, luxury real estate can become a more tax-efficient part of a long-term wealth strategy.

Whether you want to buy, sell, or rent luxury property in Puerto Rico, expert guidance is essential in today’s changing tax environment. Christie’s International Real Estate Puerto Rico helps clients evaluate premium homes, investment opportunities, and luxury properties for rent with local market insight. Contact our team today to explore Puerto Rico’s most exclusive real estate opportunities.

FAQs

Does OBBBA change the 3.8% Net Investment Income Tax (NIIT) on rental income?

No. OBBBA does not eliminate NIIT; high-income investors may still owe the 3.8% surtax on net investment income, depending on how the rental activity is classified and their overall income profile.

Will 100% bonus depreciation create “recapture” tax when I sell a luxury rental?

Potentially. Accelerated depreciation can increase depreciation recapture (often taxed up to 25% federally) and may reduce your adjusted basis, so the exit tax profile can look very different than the year-one tax savings.

How does OBBBA affect foreign buyers who own U.S. luxury real estate?

Many headline benefits are limited by nonresident rules. Foreign owners can face FIRPTA withholding on sales, different estate tax thresholds than U.S. citizens/residents, and treaty-specific outcomes—so structuring should be reviewed before acquisition.