Act 38‑2026, signed on March 10, 2026, amended Puerto Rico’s Resident Individual Investor provisions under Act 60. The law states that it became effective immediately upon approval, although legal advisers have noted that its implementation remains subject to review under PROMESA by Puerto Rico’s Financial Oversight and Management Board.

Act 38-2026 extends the Resident Individual Investor program for qualifying future applicants through December 31, 2055. Existing Act 22 and pre-2027 Act 60 decrees generally retain their original benefits through December 31, 2035, unless revoked or voluntarily modified to adopt the new post-2026 framework.

This article breaks down exactly what changed, how it affects your tax exposure, and what actions each type of investor should consider now.

Key Takeaways

December 31, 2026 determines access to the 0% vs 4% tax regime.

Pre-2027 applicants retain 0% tax on qualifying Puerto Rico-source investment income.

Post-2026 applicants face a 4% fixed tax rate plus stricter residency rules.

Existing decree holders remain grandfathered under current terms through 2035.

Principal residence ownership and bona fide residency are now more tightly enforced.

What Act 38-2026 Actually Changed for Act 60 Resident Individual Investors

Act 38-2026 did not eliminate the Puerto Rico resident investor decree—it restructured who qualifies for the best version of it. The law draws a hard line at December 31, 2026, creating two separate tracks with different tax outcomes, different eligibility conditions, and different compliance obligations. If you are evaluating your position under the Puerto Rico Act 60 changes in 2026, here is what has changed.

The following breakdown covers the core changes across four dimensions: tax rates, decree timelines, residency and property rules, and grandfathering protections.

Tax Rate Changes

Pre-2027 applicants (filed by Dec 31, 2026): Applicants who file on or before December 31, 2026 generally remain eligible for the existing exemption framework, including qualifying interest, dividends, and post-residency capital gains recognized within the applicable period ending December 31, 2035.

Post-2026 applicants (filed Jan 1, 2027 or later): Applicants filing on or after January 1, 2027 generally enter a new framework imposing a preferential 4% Puerto Rico income-tax rate on qualifying interest, dividends, and post-residency capital appreciation through December 31, 2055, unless a more favorable rate applies under another provision of law.

The Puerto Rico 4% tax rate under the new Individual Resident Investor tax framework is still far below U.S. federal rates, but it represents a meaningful shift from the prior 0% structure.

Income sourced outside Puerto Rico continues to follow standard U.S. federal tax rules, regardless of when you apply.

Decree Timelines and Program Extension

The Individual Resident Investor program’s sunset date has been extended so that new benefits can run through December 31, 2055, rather than ending in 2035.

Existing decrees under Act 22 or Act 60 remain in force on their current terms—generally through December 31, 2035—unless they are revoked or the holder renegotiates the decree to adopt the new regime.

Act 38 distinguishes between applications filed on or before December 31, 2026 and those filed from January 1, 2027 onward. Applicants approaching the deadline should confirm with the Office of Incentives and Puerto Rico tax counsel what documentation, payment and submission steps are required for an application to be treated as timely filed.

New Residency and Property Ownership Requirements

Post-2026 applicants must confirm they were not Puerto Rico residents during the six years preceding their application—a rule designed to prevent cyclical moves in and out of the island.

All applicants must purchase a principal residence in Puerto Rico within 2 years of the grant of the decree.

For applications filed on or after January 1, 2027, the principal residence must be registered, or pending registration, in the investor’s name, jointly with the investor’s spouse, or in the name of a qualifying trust described in Act 60. Earlier decree holders should review the ownership requirements contained in their particular decree and the version of law applicable to them.

Federal bona fide residency generally requires satisfying the presence test, tax-home test, and closer-connection test under Sections 933 and 937 of the Internal Revenue Code. Spending at least 183 days in Puerto Rico is one way to satisfy the presence test, but federal regulations provide additional presence-test alternatives.

Annual charitable donation requirements remain in place and continue to apply to all decree holders.

Grandfathering Rules

Decree holders who obtained their Puerto Rico investor tax decree requirements under the prior Act 22 or early Act 60 regime retain their existing terms.

The 0% rate on qualifying income applies to those grandfathered holders for the life of their decree. Under current guidance, those decrees typically run through December 31, 2035, unless they are revoked or amended to adopt the new framework.

Existing Act 22 holders and qualifying Act 60 applicants who filed on or before December 31, 2026 may request a decree modification adopting the new provisions. Doing so may replace the remaining 0% treatment under the existing decree with the 4% framework extending through 2055, so the comparative tax effect should be reviewed carefully with Puerto Rico tax counsel.

The table below summarizes the two regimes side-by-side for quick reference.

With the structural changes now clear, the next logical question is how these changes affect investors based on their current situation.

Scenario-Based Breakdown: Where Do You Stand?

The impact of Act 38-2026 varies depending on whether you already hold a decree, are mid-application, or are still deciding whether to relocate. Each scenario carries different risks and different actions worth considering. The Puerto Rico tax incentives under Act 60 remain among the most attractive in the U.S. territory system—but only if you approach them correctly.

Scenario 1: You Already Hold an Act 60 or Act 22 Decree

If you hold an existing Puerto Rico resident investor decree, Act 38-2026 does not immediately change your tax rate or compliance obligations. Your decree terms are grandfathered, and you continue to benefit from the 0% rate on qualifying Puerto Rico-source income as long as you remain in compliance.

That said, there are real risks to watch.

Do not modify, surrender, or restructure an existing decree without comparing the remaining value of the 0% benefits through 2035 against the potential availability of the 4% framework through 2055.

Confirm that the ownership and registration of your principal residence satisfy the terms of your decree and the law applicable to your filing date, particularly before transferring the property to or from an entity or trust.

Maintain detailed records supporting the applicable federal presence test, as well as your Puerto Rico tax home and closer connection.

Keep annual charitable donation records up to date and documented.

Consult a Puerto Rico tax attorney before making any structural changes to how you hold your residence or business assets.

Scenario 2: You Are Applying Before December 31, 2026

This is perhaps the most time-sensitive position. If you file a qualifying application on or before December 31, 2026, you generally preserve access to the existing exemption framework through December 31, 2035, subject to the decree’s terms and continued compliance. The 2055 period applies to the new framework, which generally carries a 4% preferential rate rather than the existing 0% treatment.

Here is what to prioritize if you are in this position.

Confirm your application is complete and submitted—not just initiated—before December 31, 2026.

Coordinate the decree application with a documented relocation plan addressing the federal presence, tax-home and closer-connection tests. The timing of Puerto Rico residency and the application should be confirmed with qualified tax counsel because they are related but not identical legal requirements.

Begin identifying your principal residence in Puerto Rico, since you must purchase one within two years of the decree grant.

Work with a qualified Puerto Rico tax attorney to structure your assets correctly before the decree is issued.

Avoid holding your future primary residence through a corporation or LLC—only personal, joint spousal, or eligible trust ownership qualifies.

Scenario 3: You Are Still Deciding Whether to Relocate

If you have not yet committed to relocating, Act 38-2026 raises the cost of waiting. An application filed on or after January 1, 2027 generally falls under the new 4% preferential framework, although Act 38 preserves the use of a more favorable rate when another applicable provision of Puerto Rico law provides one. For high-net-worth individuals with significant capital gains exposure, that difference compounds meaningfully over time.

A few points are worth careful thought.

The 4% Puerto Rico rate remains preferential compared with ordinary Puerto Rico income-tax treatment, but an investor’s total federal, territorial and state tax result depends on residency, income sourcing, pre-move appreciation and the investor’s individual circumstances.

For applications filed after December 31, 2026, the applicant must generally demonstrate that the applicant was not a Puerto Rico resident during the six years preceding the move to Puerto Rico. Prior Puerto Rico residents should obtain advice on how that lookback period applies to their specific dates and residency history.

The program's extension to 2055 means there is still a long runway, but the best terms belong to those who act before the end of 2026.

Purchasing and maintaining a qualifying principal residence in Puerto Rico is a decree requirement, although the law does not require the residence to be a luxury property. Buyers should verify the purchase timing, seller relationship, title structure and actual use of the property before relying on it for compliance.

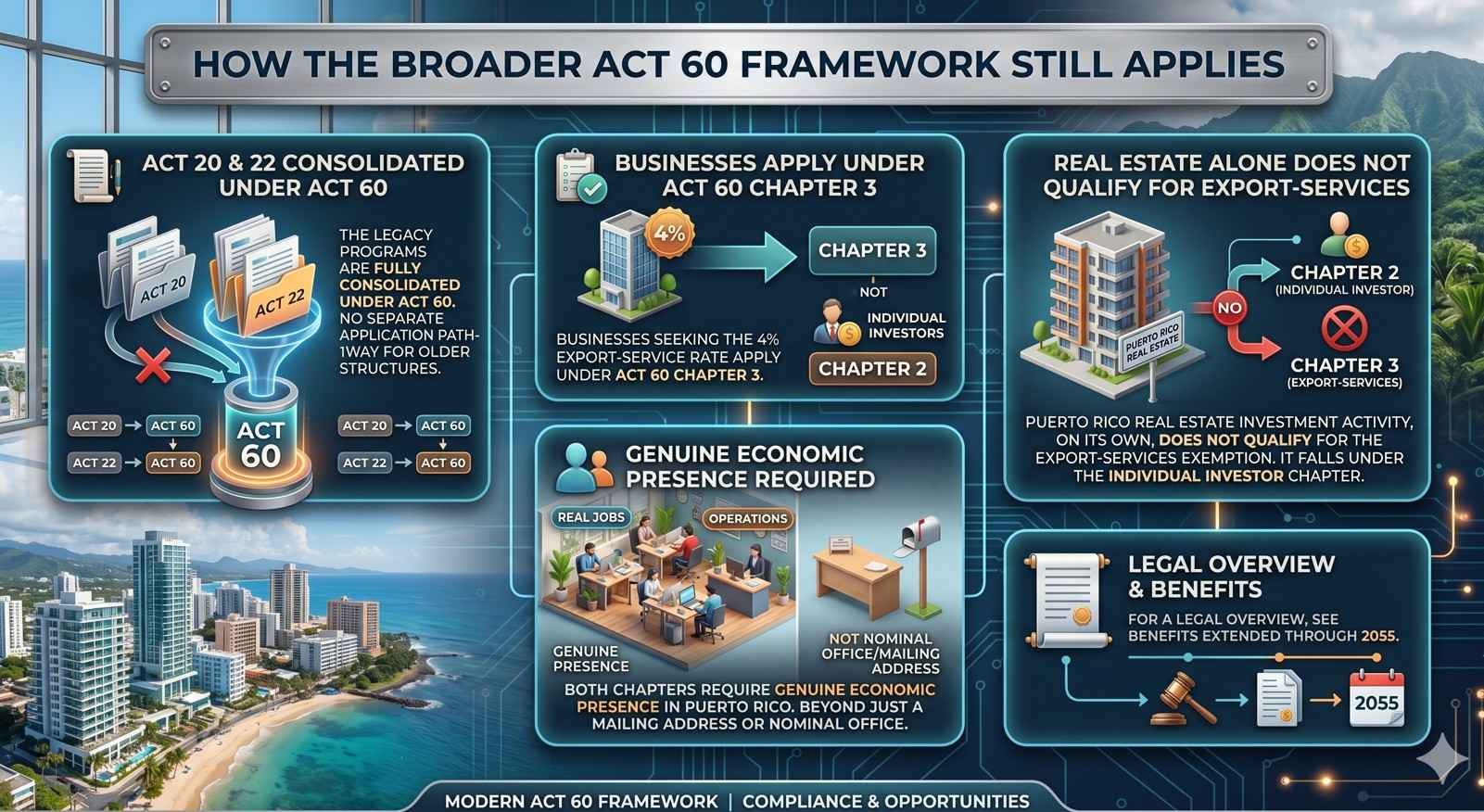

How the Broader Act 60 Framework Still Applies

The Puerto Rico Act 60 changes in 2026 focus specifically on the Resident Individual Investor chapter. The export services chapter—formerly Act 20—remains largely intact and continues to offer a 4% corporate tax rate on qualifying export-service business income. If you operate a service business that can be relocated to Puerto Rico, that incentive still applies, independent of the individual investor decree changes.

The full Act 60 framework also continues to provide substantial exemptions on Puerto Rico dividends and property taxes for qualifying businesses, making the island attractive to entrepreneurs and service-sector operators as well as pure investors.

The Act 20 and Act 22 legacy programs are now fully consolidated under Act 60—there is no separate application pathway for those older structures.

Businesses seeking the 4% export-service rate apply under Act 60 Chapter 3, not Chapter 2 (which governs individual investors).

Both chapters require genuine economic presence in Puerto Rico—not just a mailing address or nominal office.

Puerto Rico real estate investment activity, on its own, does not qualify for the export-services exemption—it falls under the individual investor chapter.

Compliance Risks High-Net-Worth Investors Should Watch

IRS scrutiny of Puerto Rico bona fide residency claims has intensified in recent years, and Act 38-2026 further tightens the rules, creating new compliance pressure points. Investors who treat their Puerto Rico decree as a paperwork exercise rather than a genuine relocation face real audit risk.

The following are the most common compliance vulnerabilities worth addressing proactively.

Presence documentation: Maintain clear, contemporaneous records supporting the federal presence test you rely on, including travel records, lodging information, financial transactions and other location evidence.

Principal place of business: A continuing tax home or stronger personal and economic connection outside Puerto Rico may undermine bona fide residency even when an investor has substantial physical presence on the island.Closer connection test: You must demonstrate a closer connection to Puerto Rico than to any other jurisdiction—this includes where your family lives, where you maintain social ties, and where your professional relationships are concentrated.

Residence ownership structure: Under Act 38-2026, the requirement that your principal residence be owned personally (or jointly with spouse or eligible trust) is explicit—review how you currently hold your Puerto Rico property.

Charitable donation records: Annual donations are a decree condition—keep documentation current and consistent.

Puerto Rico Luxury Properties for Sale

For investors pursuing an Act 60 decree—whether before or after the 2026 deadline—purchasing a qualifying principal residence is not optional. It is a legal requirement, and the quality of that property matters for both compliance and long-term value. Christie's International Real Estate Puerto Rico specializes in connecting high-net-worth buyers with luxury properties for sale across the island's most sought-after markets, from Dorado Beach to Culebra.

Whether you are buying to satisfy decree requirements or simply looking for Puerto Rico luxury real estate that reflects your standard of living, the listings below represent some of the finest options currently available.

17 Dorado Beach Estates, Dorado, PR 00646

This exceptional estate sits within the prestigious Dorado Beach resort community, one of Puerto Rico's most exclusive addresses for high-net-worth residents and decree holders. The property combines resort-level amenities with the privacy and ownership structure that qualifies under Act 60 principal residence requirements.

49 Los Lagos, Humacao, PR 00791

Set within the tranquil Los Lagos community in Humacao, this property offers a refined residential experience on Puerto Rico's eastern coast. It presents a strong option for investors seeking Puerto Rico luxury homes outside the metropolitan core while maintaining easy access to key business and lifestyle amenities.

17 Calle Durazno, Urbanización San Patricio, Guaynabo, PR 00968

Located in the well-established Urbanización San Patricio neighborhood in Guaynabo, this home offers proximity to San Juan's financial and business districts—a practical consideration for decree holders who need to demonstrate a principal place of business in Puerto Rico. The property's location and structure make it a natural fit for investors building genuine, long-term residency on the island.

Bo Flamenco Las Quintas Solar 15, Culebra, PR 00775

This rare Culebra land parcel sits near the world-renowned Flamenco Beach, offering an extraordinary opportunity to build a bespoke principal residence in one of Puerto Rico's most unspoiled island settings. For investors who want their Act 60 principal residence to double as a long-term lifestyle asset, few locations on the island match Culebra's combination of natural beauty and exclusivity.

Final Thoughts

Act 38-2026 reshapes the Act 60 investor landscape by splitting applicants into pre- and post-2027 regimes with materially different tax outcomes. Act 38-2026 distinguishes between applications filed by December 31, 2026, which generally remain under the existing exemption framework through 2035, and applications filed from January 1, 2027 onward, which generally enter a 4% preferential framework extending through 2055. Existing decree holders and certain pre-2027 applicants may be able to elect the new framework through a decree modification, but that decision requires a comparison of the remaining 0% period against the longer 4% period.

Whether you are planning to relocate or already navigating Act 60, securing the right property is a critical step. Christie's International Real Estate Puerto Rico offers exclusive access to premier luxury homes in Puerto Rico that meet decree requirements and long-term lifestyle goals. Connect with their team to buy, sell, or rent with confidence in Puerto Rico’s high-end market.

FAQs

Does an Act 60 application need to be filed or approved by December 31, 2026?

Act 38 classifies applicants according to when the application is filed, not merely when the decree is ultimately approved. Because the law does not resolve every administrative question about incomplete or deficient submissions, applicants should confirm the filing requirements with the Office of Incentives and Puerto Rico counsel before the deadline.

What counts as “Puerto Rico-source” investment income for the 0%/4% rates?

Sourcing depends on the specific asset and the location of the underlying issuer, activity, or property. Because sourcing determines whether the incentive rate applies, investors should confirm the treatment for each income stream (e.g., securities, partnership interests, real estate) with Puerto Rico tax counsel.

Can I buy a home first and apply for the decree later?

You can purchase property before applying, but the decree requirement is to own a qualifying principal residence within two years after the decree is granted—so buying early doesn’t extend the post‑grant deadline or replace the need to satisfy residency and other decree conditions.