Puerto Rico's 2025–2026 legislative package — spanning Act 38-2026, Act 60 extensions, OBBBA Opportunity Zone updates, Act 180-2025 capital gains revisions, and Act 106 permitting reform — has fundamentally shifted the calculus for luxury property investors on the island. These changes affect tax rates, residency compliance, development timelines, and capital allocation in ways that demand immediate attention.

This article walks both prospective buyers and current Act 60 participants through each change and what it means for their investment decisions.

Key Takeaways

Act 38-2026 creates a major deadline for new Act 60 applicants.

Future Act 60 participants may face a 4% tax rate after 2026.

Opportunity Zone and Act 60 planning now require closer coordination.

Act 106 may improve permitting timelines for luxury development projects.

Puerto Rico luxury real estate investors should act with stronger timing, documentation, and professional guidance.

Key 2025–2026 Laws Impacting Puerto Rico Luxury Investors

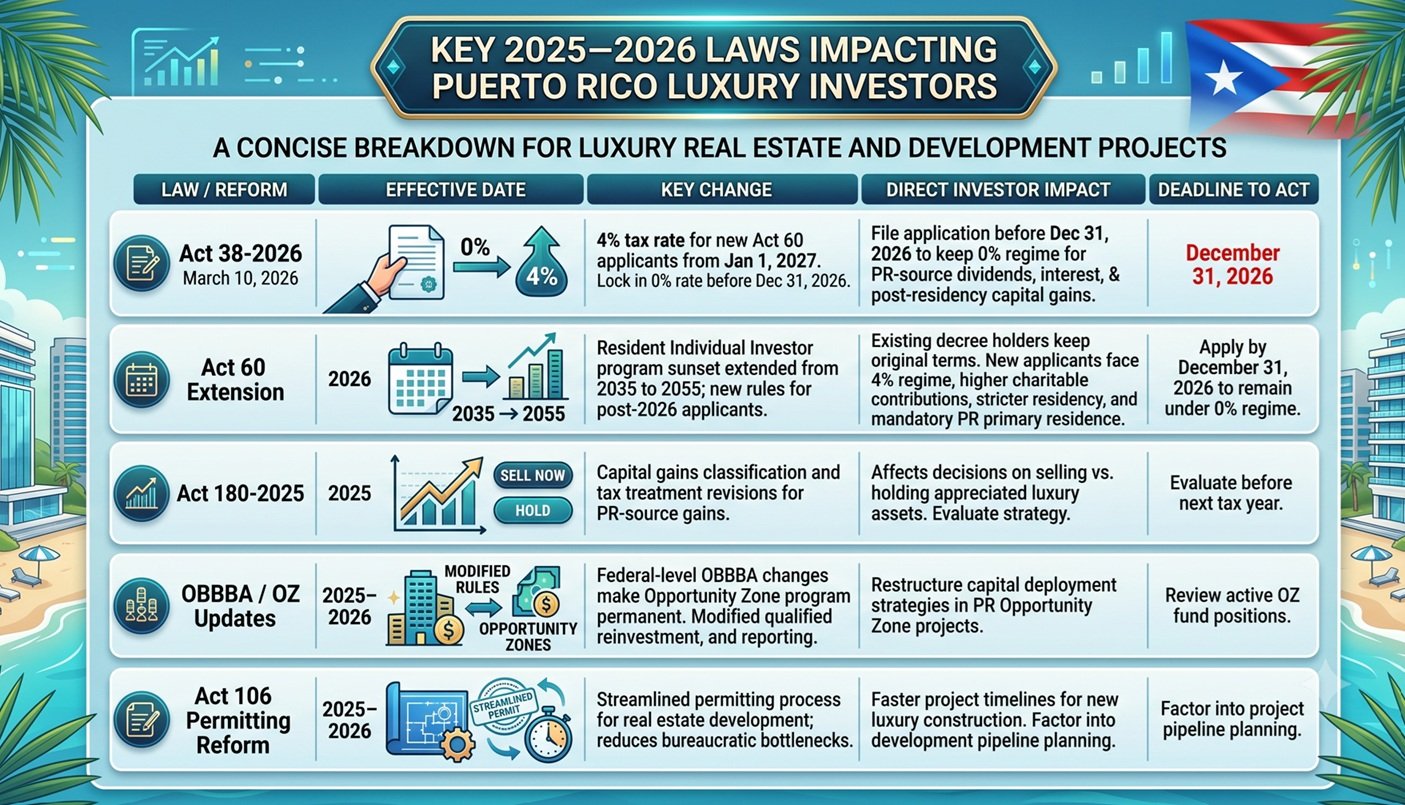

The 2025–2026 legislative cycle produced a cluster of laws that touch nearly every stage of a luxury property investment — from acquisition and tax structuring to permitting and exit strategy. Understanding each one in isolation is useful, but the real strategic value comes from seeing how they interact with each other and with your specific investment timeline.

Here is a concise breakdown of each law and its direct implications for investors in Puerto Rico luxury homes and development projects.

Act 38-2026 (signed March 10, 2026): Amends the Act 60 Incentives Code for Resident Individual Investors. New applicants who submit their decree application after December 31, 2026, are subject to a 4% income tax rate on Puerto Rico‑source dividends, interest, and post‑residency capital gains, while applications filed on or before December 31, 2026, generally remain under the existing 0% regime for these items. Current decree holders keep their original terms unless they opt to amend their decree to adopt the new framework.

Act 60 Extension Framework: Act 38‑2026 extends the Resident Individual Investor program’s sunset from 2035 to 2055, while maintaining the original terms for existing decrees unless they are amended or revoked. New compliance conditions include higher mandatory charitable contributions, stricter bona fide residency requirements, and a mandatory primary-residence purchase in Puerto Rico.

Act 180-2025 (Capital Gains Revisions): Introduced changes to how Puerto Rico-source capital gains are classified and taxed at the territorial level. This affects investors holding appreciated assets — particularly luxury properties — who are evaluating whether to sell before or after the new rules take full effect.

OBBBA and Opportunity Zone Updates: Federal‑level adjustments through the One Big Beautiful Budget Act have modified and made permanent the Opportunity Zone program, including changes to qualified property definitions, reinvestment timelines, and reporting requirements. These changes affect how developers and investors structure capital deployment into Puerto Rico Opportunity Zone projects.

Act 106 Permitting Reform: Streamlines the permitting process for real estate development in Puerto Rico. The reform reduces bureaucratic bottlenecks that previously added months — sometimes over a year — to new construction timelines. This directly affects investors in new construction luxury properties across coastal and urban markets.

The table below summarizes the key parameters of each law side by side, so you can quickly assess which changes are most relevant to your current position.

With this overview in place, the next sections examine each change in detail and tie each one directly to the decisions you are likely weighing right now.

New 4% Tax for Future Act 60 Participants

Act 38-2026 is perhaps the most time-sensitive change in this legislative cycle for anyone considering Puerto Rico luxury real estate as part of a tax relocation strategy. The law draws a clear line:

Applications filed by December 31, 2026, remain eligible for the 0% preferential rate on Puerto Rico-source dividends, interest, and post-residency capital gains, while

Those filed on or after January 1, 2027, will be subject to a 4% rate

That 4% figure may sound modest, but for investors managing eight- or nine-figure portfolios, the cumulative difference over a 10-year decree period is substantial.

The grandfathering provisions in Act 38‑2026 protect current decree holders, who generally retain their original 0% treatment on interest, dividends, and post‑residency capital gains through their existing decree term unless they choose to amend it, which signals that Puerto Rico is preserving prior commitments while repricing entry for future participants.

What This Means for Buyers Considering Act 60 Now

If you have been evaluating an Act 60 application but have not yet filed, the December 31, 2026, deadline is a hard cutoff, not a soft guideline.

Filing before the deadline also means you must meet the mandatory primary-residence purchase requirement, which makes acquiring Puerto Rico luxury homes a compliance necessity, not just a lifestyle choice.

The stricter bona fide residency rules under the updated framework require more documented presence on the island, so your property acquisition strategy and physical calendar need to align.

Investors who are already residents but have not yet filed for a decree should treat this as the most urgent item on their 2026 financial planning list.

Buy Now vs. Wait — The Tax Math

A 0% rate on capital gains versus a 4% rate is a permanent structural difference for the life of your decree.

For an investor with $50 million in appreciated assets planning to sell over a 10-year horizon, the difference between 0% and 4% on gains realized in Puerto Rico could easily exceed $2 million in aggregate tax liability.

Waiting until 2027 to apply does not just cost you the rate differential — it also means navigating a new compliance environment that is still being interpreted by practitioners and regulators.

In practice, the period up to December 31, 2026, is the last opportunity for new Resident Individual Investors to apply under the current 0% regime for dividends, interest, and post‑residency capital gains before the 4% framework applies to later applicants.

Act 60 Extension and Tighter Compliance Conditions

The extension of the Resident Individual Investor framework to 2055 under Act 38‑2026 confirms that Puerto Rico’s commitment to attracting high‑net‑worth investors is long-term, not a short‑term experiment. That said, the updated compliance conditions signal a meaningful shift in what the government expects from decree holders going forward. Higher mandatory charitable contributions, stricter residency documentation, and the primary-residence purchase requirement are not token changes — they reflect a deliberate effort to ensure that Act 60 participants are genuinely integrated into the local economy.

For investors already holding decrees, the grandfathering provision provides stability, but it does not eliminate the need for ongoing compliance review.

Compliance Areas That Deserve Immediate Attention

Residency documentation: The updated bona fide residency standard requires more than just owning a home in Puerto Rico. You need to demonstrate genuine ties — days present, social connections, business activity on the island.

Charitable contribution thresholds: The new minimums are higher than what earlier decree holders may have budgeted. Review your annual giving plan against the updated requirements.

Primary residence ownership: If you currently rent your Puerto Rico home rather than own it, the updated rules create a direct incentive — and in some cases, a requirement — to purchase. This is where the Puerto Rico luxury real estate market becomes directly relevant to your compliance strategy.

Decree renewal and amendment filings: Some existing decree holders may need to amend their decrees to reflect updated personal or business circumstances. Delays in doing so can create compliance gaps.

OBBBA and Opportunity Zone Adjustments

Image Source: tax1099.com

The federal One Big Beautiful Budget Act introduced modifications to the Opportunity Zone program that affect how investors structure capital deployment into Puerto Rico OZ projects. The changes touch qualified property definitions, reinvestment timelines, and the treatment of gains deferred through Qualified Opportunity Funds. For developers and investors active in Puerto Rico luxury real estate development — particularly in designated OZ census tracts across San Juan, Ponce, and coastal municipalities — these adjustments require a fresh look at existing fund structures and project timelines.

Opportunity Zone changes in Puerto Rico intersect directly with the Act 60 framework, creating a layered tax planning environment that rewards careful structuring.

Key Adjustments Under the OBBBA

Modified definitions of "substantially all" for qualified OZ business property may affect whether certain luxury development projects meet the threshold for preferential treatment.

Updated reinvestment timelines give investors more flexibility in some cases, but also introduce new documentation requirements that must be tracked carefully.

The interaction between OZ gains deferral and Act 60 capital gains treatment creates planning opportunities — but only if the two frameworks are coordinated properly from the outset.

Investors holding OZ fund interests should review whether their underlying Puerto Rico projects still qualify under the revised rules, particularly if property use or development scope has changed since the original fund formation.

Capital Allocation Decisions in an Adjusted OZ Environment

Projects in Puerto Rico OZ tracts that were structured under pre-OBBBA rules may need to be restructured to preserve their tax-advantaged status.

New OZ investments should be underwritten with the updated rules as the baseline, not the prior framework.

The combination of OZ benefits and Act 60 treatment — when properly structured — still represents one of the most favorable tax environments for real estate capital deployment available anywhere in the United States.

If you are evaluating a new development investment in Puerto Rico luxury real estate, the OZ designation of the target parcel should be one of the first items your legal and tax team reviews.

Act 180-2025 and Capital Gains Timing Decisions

Act 180‑2025 introduced a targeted capital gains tax exemption for the sale of a taxpayer’s principal residence in Puerto Rico, which directly affects how homeowners and some investors time the sale of a high‑value primary home on the island.

The law's changes to gain classification affect how different categories of appreciation are treated, which in turn affects the net after-tax return on a sale. Puerto Rico capital gains tax 2025 planning has become a more nuanced exercise than it was even two years ago. The practical effect for luxury property holders is that the timing of a sale now carries more weight than it did under the prior rules.

Sell Now, Hold, or Exchange — How Act 180-2025 Affects the Decision

Investors who acquired Puerto Rico luxury homes before establishing Act 60 residency need to carefully distinguish between pre-residency and post-residency appreciation — the tax treatment differs, and Act 180-2025 affects how that line is drawn.

For current Act 60 holders, post-residency gains on Puerto Rico-source assets remain subject to preferential treatment, but the classification rules under Act 180-2025 require precise documentation of acquisition dates, cost basis, and improvement expenditures.

A 1031-style exchange at the territorial level — where available — may allow investors to defer gain recognition while repositioning capital into higher-value Puerto Rico luxury properties without triggering an immediate tax event.

Investors planning to sell appreciated beachfront or urban luxury properties should model the after-tax proceeds under both the pre- and post-Act 180-2025 framework before executing a transaction.

Permitting Reform and Development Timelines Under Act 106

Act 106 permitting reform addresses one of the most persistent friction points in Puerto Rico real estate development — the time and unpredictability of the permitting process. Before this reform, developers of luxury properties in Puerto Rico often faced permitting timelines that stretched 12 to 18 months or longer, creating carrying cost overruns and financing complications that eroded project returns.

The reform streamlines agency review processes, introduces clearer timelines for government responses, and reduces the bureaucratic layering that previously slowed approvals.

How Faster Permitting Changes the Investment Case

Shorter permitting timelines reduce the carrying cost period between land acquisition and construction start, which improves project-level IRR for development investments.

More predictable approval timelines make it easier to underwrite financing structures and commit to delivery schedules — both of which matter to institutional and family office capital that has historically been cautious about Puerto Rico development risk.

Puerto Rico permitting reform under Act 106 also benefits buyers of off-market new construction properties, since developers can bring projects to market faster and with greater cost certainty.

Investors with active development pipelines should re-run their project pro formas with updated permitting timeline assumptions — the improvement in timeline predictability may materially change the attractiveness of projects that were previously borderline.

Markets Most Affected by Permitting Reform

Dorado: High-value beachfront and golf-community developments stand to benefit most, given the complexity of coastal permitting that previously created the longest delays.

Condado and Miramar: Urban luxury condominium and mixed-use projects will see faster approvals, which supports the continued growth of the Puerto Rico luxury real estate market in San Juan's premier neighborhoods.

Rincon and the West Coast: Boutique luxury developments in surf and lifestyle markets have faced permitting unpredictability for years — Act 106 should reduce that variability.

What Investors Should Do Now

The 2025–2026 legislative changes create a clear set of strategic priorities for anyone with capital deployed — or planning to deploy capital — in Puerto Rico luxury real estate. The window to act under the most favorable conditions is narrowing, and the decisions you make in the next 6 to 12 months will shape your tax position and investment returns for the next decade.

Christie's International Real Estate Puerto Rico works directly with investors navigating exactly this kind of environment, connecting financial strategy with on-the-ground market access across Dorado, Condado, Old San Juan, and the island's most exclusive coastal markets. Here are the specific moves that deserve your attention right now.

File your Act 60 application before December 31, 2026, if you have not already done so. The 0% rate is available now. The 4% rate starts January 1, 2027. This is the single most time-sensitive item on this list.

Review your bona fide residency documentation against the updated standards under Act 38-2026. If your days-on-island count or local ties are thin, address that before your next compliance review.

Audit your charitable contribution plan to confirm it meets the updated thresholds. This is a straightforward compliance item that some decree holders overlook until it becomes a problem.

Model your capital gains position under Act 180-2025 before selling any appreciated Puerto Rico assets. The classification rules matter, and the difference between getting this right and getting it wrong is measurable in real dollars.

Review active OZ fund positions against the updated OBBBA rules. If your underlying Puerto Rico projects have changed scope or use since fund formation, confirm they still meet qualified property standards.

Re-evaluate your development project pipeline with updated permitting timeline assumptions under Act 106. Projects that looked marginal under the old timeline may now pencil out.

Engage a Puerto Rico-based legal and tax team that is current on all five of these legislative changes. The interaction effects between them require coordinated advice, not siloed analysis.

To explore luxury properties in Puerto Rico that align with your Act 60 compliance requirements or development investment criteria, contact a specialist at Christie's International Real Estate Puerto Rico.

Luxury Properties and Houses for Sale in Puerto Rico

With legislative support reinforcing long-term investment potential, now is an ideal time to explore luxury houses for sale across Puerto Rico’s most sought-after regions. At Christie's International Real Estate Puerto Rico, we specialize in helping discerning buyers transition seamlessly into island living while securing the finest properties that align with their lifestyle and investment goals. Below, you’ll find our curated listings of luxury properties that exemplify the unique opportunities currently available on the island.

934 ISLA NORTE DORADO PR, 00646

Set in Isla Norte within Sabanera Dorado, this 2023-built modern home offers about 5,100 SF of refined living with 4 bedrooms including 3 ensuite, 4 full and 2 half baths with a distinctive outdoor bath, and a resort-style backyard with pool, terrace, grill area, and lush landscaping, plus designer furnishings, covered garage parking, 24/7 security, club amenities, and quick access to TASIS.

2019 CACIQUE ST SAN JUAN PR, 00911

Located steps from Ocean Park Beach, this multifamily San Juan property offers five units and strong income potential in a desirable coastal neighborhood.

152 SAN JUSTO ST, SAN JUAN PR, 00901

Located in Old San Juan’s vibrant historic district, this 10-unit building presents a high-value rental investment near cafes, museums, and cultural landmarks.

#1 LOS LAGOS HUMACAO PR, 00791

This one-level corner home in Los Lagos at Palmas del Mar offers 5,600 SF with 4 bedrooms, 3.5 baths, lake and golf views, a private pool, covered BBQ terrace, full generator, and a fully fenced 24/7 gated setting with resort-style community amenities and direct access to everything Palmas del Mar offers.

Conclusion

Puerto Rico’s 2025–2026 legislative changes create new urgency for luxury property investors, especially those relying on Act 60, Opportunity Zones, or development timelines. Buyers and developers should review tax deadlines, residency rules, capital gains planning, and permitting assumptions before making major investment decisions. With the right legal, tax, and real estate guidance, Puerto Rico luxury real estate can still offer strong long-term value under the updated rules.

Looking to buy, sell, or rent luxury property in Puerto Rico? Christie's International Real Estate Puerto Rico helps high-net-worth buyers and investors navigate premium properties, compliance-driven purchases, and strategic market opportunities. Connect with our team today to explore Puerto Rico luxury properties that align with your lifestyle, tax planning, and investment goals.

FAQs

What types of real estate properties qualify as luxury investments in Puerto Rico?

Luxury investments in Puerto Rico typically include beachfront estates, modern penthouses, gated community villas, and upscale urban condos located in prime real estate locations such as Dorado, Condado, and Isla Verde. These premium properties often feature luxury amenities like private pools, security systems, and resort-style living. When you invest in luxury property, you’re entering a segment of the real estate market known for stability, exclusivity, and long-term value growth.

How do the latest legislative changes influence luxury rental opportunities in Puerto Rico?

The new laws support luxury rental demand by incentivizing developers to create more high-end real estate options in revitalized city zones. This increases investment opportunities for buyers seeking to generate income through rental properties, particularly in areas where tourism and demand for luxury are surging. Investors can focus on luxury properties with features that appeal to long-term tenants or high-end vacationers.

Does filing an Act 60 application by December 31, 2026 guarantee approval under the 0% regime?

No. Filing by the deadline preserves eligibility for the 0% terms, but approval still depends on meeting all program requirements (including documentation, residency-related conditions, and any updated decree obligations) and receiving the decree. For updates on the Act 60 resident investor program, consult current guidance.

How should investors coordinate U.S. federal taxes with Puerto Rico incentives before buying?

Build a two-jurisdiction plan that aligns Puerto Rico residency timing, sourcing rules, and entity structure with U.S. federal reporting (e.g., information returns and anti-deferral regimes where applicable). Your U.S. CPA and Puerto Rico tax counsel should review the structure before you close or move.

What due diligence is most important when buying a luxury property for compliance and resale?

Confirm clean title and permits, validate zoning/coastal restrictions, document purchase date and improvement costs for basis tracking, and ensure the property can function as a bona fide primary residence (utilities, occupancy evidence, and local ties) to support future compliance reviews. For broader Puerto Rico real estate legal context, review a current practice guide.