Current market factors shaping luxury home financing in Puerto Rico include shifting buyer demand, lender risk requirements, and insurance and regulatory pressures that can influence both rates and approval timelines.

Financing luxury homes in Puerto Rico presents unique challenges that mainland buyers rarely encounter. Most US banks refuse to lend on Puerto Rico collateral, forcing buyers to navigate a smaller pool of local lenders with stricter requirements. Down payments typically range from 30-40% for luxury properties, and closing timelines are 45-90 days, compared with mainland transactions.

Key Takeaways

- Most luxury financing in Puerto Rico is handled by local banks rather than by mainland U.S. lenders.

- Expect larger down payments (typically 30–40%) and stricter documentation requirements.

- Jumbo and higher-end loans can be capped, so some buyers use private or asset-based lending.

- Closings usually take longer (about 45–90 days) because due diligence and local clearances add steps.

Local vs. US Lenders: Understanding the Puerto Rico Mortgage Landscape

Image Source: newsroom.popular.com

Mainland US banks typically avoid financing property in Puerto Rico due to regulatory complexities and perceived risk factors. This limitation forces luxury home buyers to establish relationships with local financial institutions that understand the island's unique legal and economic environment. The disconnect between mainland and local lending creates a more concentrated market with fewer financing options.

The major players dominating the Puerto Rico mortgage market include Banco Popular, FirstBank, and Oriental Financial Group. These institutions control the majority of luxury home financing and often require established banking relationships before approving large loans.

Primary Local Lenders

- Banco Popular de Puerto Rico - The island's largest bank with extensive luxury property lending experience

- FirstBank Puerto Rico - Strong presence in high-end residential financing

- Oriental Financial Group - Competitive rates for qualified borrowers

- Citibank Puerto Rico - Limited luxury lending but established presence

Note: While Scotiabank was historically a major lender on the island, it exited the market after selling its Puerto Rico operations to Oriental Bank in 2019. Consequently, buyers seeking Scotiabank mortgage products or services are now managed entirely through Oriental Financial Group.

Why US Banks Avoid Puerto Rico

- Complex local regulations and legal framework differences

- Currency and economic stability concerns

- Limited ability to efficiently service loans from mainland offices

- Unfamiliarity with local property valuation methods

- Challenges with foreclosure processes under Puerto Rico law

Jumbo Loan Requirements and Criteria

Jumbo loans Puerto Rico operate under different thresholds and requirements compared to mainland markets. Properties exceeding $832,750 fall into jumbo loan territory, though luxury homes in prime locations like Dorado Beach or Condado often require financing well above this amount. Local lenders typically cap jumbo loans at $2-3 million, requiring alternative financing structures for higher-priced properties.

The approval process demands extensive financial documentation and often requires borrowers to maintain significant liquid assets beyond the down payment. Credit score requirements typically start at 740 for jumbo loans, with debt-to-income ratios capped at 36%.

Loan Type | Down Payment | Credit Score | Max Loan Amount | Typical Timeline |

|---|---|---|---|---|

Conventional | 25-30% | 680+ | $832,750 | 45-60 days |

Jumbo | 30-40% | 740+ | $2-3 million | 60-90 days |

Portfolio | 40-50% | 760+ | $5+ million | 90+ days |

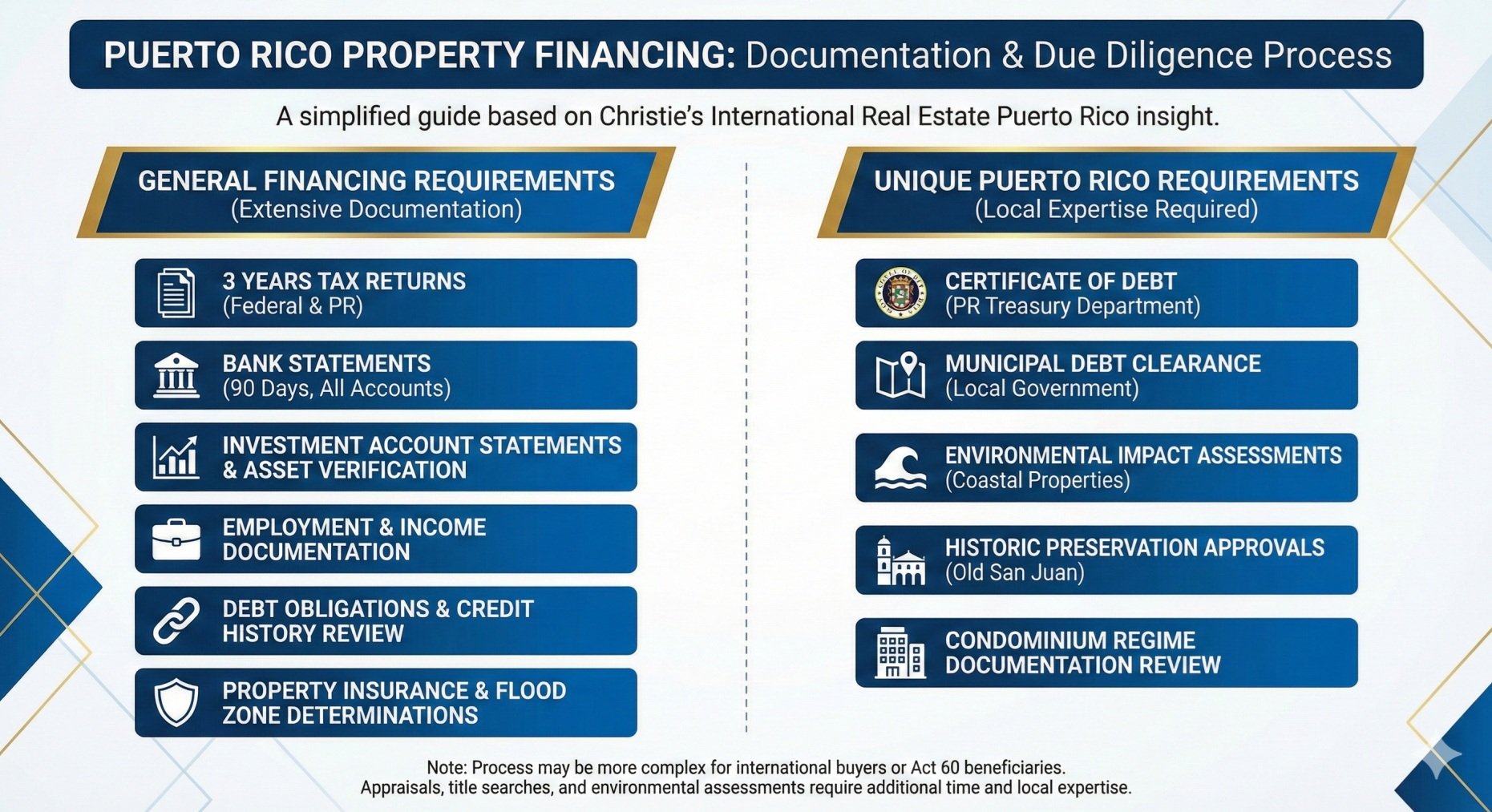

Documentation and Due Diligence Process

Financing property in Puerto Rico requires extensive documentation that exceeds typical mainland requirements. Lenders demand comprehensive financial records, tax returns from multiple jurisdictions, and detailed asset verification. The process becomes more complex for international buyers or those claiming Puerto Rico tax benefits under Act 60.

Property appraisals often take longer due to limited comparable sales data in luxury markets. Environmental assessments and title searches require local expertise and additional time for completion.

Required Documentation

- Three years of tax returns (federal and Puerto Rico if applicable)

- Bank statements from all accounts for 90 days

- Investment account statements and asset verification

- Employment verification and income documentation

- Debt obligations and credit history review

- Property insurance quotes and flood zone determinations

Unique Puerto Rico Requirements

- Certificate of Debt from the Puerto Rico Treasury Department

- Municipal debt clearance from local government

- Environmental impact assessments for coastal properties

- Historic preservation approvals for Old San Juan properties

- Condominium regime documentation review

Interest Rates and Market Conditions

Interest rates for luxury home mortgages in Puerto Rico typically run 0.25-0.75% higher than comparable mainland rates. This premium reflects the concentrated lending market and perceived additional risk factors. The Puerto Rico Home Mortgage Finance Market projects growth of 1.5% annually through 2030, driven by increased demand from mainland relocations and international investment.

Rate locks become crucial given extended closing timelines, though most lenders limit locks to 60-90 days. Borrowers often face rate renegotiation if closing delays extend beyond the initial lock period.

Current Market Factors

Positive Influences

- Increased private equity investment in Puerto Rico real estate

- Growing FinTech lending options expanding market access

- Act 60 tax incentives driving high-net-worth relocations

- Limited inventory in prime locations supporting property values

Market Challenges

- Concentrated lending market with limited competition

- Economic uncertainty affecting long-term rate projections

- Hurricane and natural disaster insurance requirements

- Regulatory changes potentially affecting tax incentive programs

Alternative Financing Strategies

High-net-worth buyers often employ creative financing structures when traditional mortgages fall short. Portfolio lending through private banks allows for customized terms and higher loan amounts, though at premium rates. Asset-based lending uses investment portfolios as collateral, enabling buyers to avoid liquidating positions for large down payments.

International buyers frequently utilize offshore financing or seller financing arrangements to navigate local lending limitations. These strategies require sophisticated legal and tax planning to ensure compliance with both US and Puerto Rico regulations.

Portfolio and Private Banking Solutions

- Relationship-based lending with flexible underwriting criteria

- Higher loan limits exceeding traditional jumbo caps

- Customized repayment terms and interest-only options

- Cross-collateralization using multiple properties or assets

International Financing Options

- Foreign bank financing for non-US citizens

- Currency hedging strategies for international buyers

- Offshore trust structures for asset protection

- Seller financing with sophisticated legal documentation

Working With US Banks in Puerto Rico for Mortgages

While most mainland banks avoid Puerto Rico mortgages, several maintain limited operations through local subsidiaries or correspondent relationships. Citibank Puerto Rico offers some luxury financing options, though with restricted loan amounts and stricter qualification requirements. These relationships often require existing banking history and substantial deposits with the institution.

The key advantage of working with US banks in Puerto Rico for mortgages lies in their ability to coordinate with mainland operations for complex financial situations. However, their limited local market knowledge can create challenges during the underwriting and closing process.

Institution Type | Advantages | Limitations | Best For |

|---|---|---|---|

Local Banks | Market expertise, faster processing | Limited loan amounts, higher rates | Standard luxury purchases |

US Bank Subsidiaries | Mainland coordination, established systems | Limited availability, strict requirements | Existing bank customers |

Private Banks | Flexible terms, high loan limits | Premium rates, relationship requirements | Ultra-high-net-worth buyers |

Asset-Based Lenders | Quick approval, portfolio collateral | Higher rates, shorter terms | Investment-heavy portfolios |

Timeline and Closing Process

Luxury home closings in Puerto Rico typically require 45-90 days from contract execution to final closing. This extended timeline reflects additional due diligence requirements, local regulatory compliance, and the limited number of qualified professionals handling high-end transactions. Buyers should plan for potential delays and maintain flexibility in their financing arrangements.

The closing process involves multiple local attorneys, notaries, and government offices that operate on island time rather than mainland business urgency. Smart buyers begin the pre-approval process before identifying specific properties to minimize delays once under contract.

Typical Closing Timeline

This typical closing timeline breaks down what most luxury home purchases in Puerto Rico look like after contract signing, from initial loan processing through due diligence and final closing.

Weeks 1-2: Initial Processing

- Mortgage application submission and initial underwriting review

- Property appraisal ordering and scheduling

- Title search initiation and preliminary report

- Insurance quotes and flood zone determinations

Weeks 3-6: Due Diligence

- Appraisal completion and review

- Environmental assessments for coastal properties

- Municipal permits and compliance verification

- Condominium documentation review and approval

Weeks 7-12: Final Approval and Closing

- Final underwriting approval and loan documentation

- Title insurance policy preparation

- Closing coordination with all parties

- Funds transfer and deed recording

Tax Considerations and Act 60 Impact

Puerto Rico's Act 60 tax incentives significantly impact luxury home financing strategies for qualifying individuals. Buyers establishing bona fide Puerto Rico residency can benefit from substantial tax savings, though lenders scrutinize these arrangements carefully during underwriting.

Mortgage interest deductibility follows federal tax rules, though Act 60 beneficiaries may find different optimization strategies compared to mainland taxpayers. Professional tax and legal advice becomes essential when coordinating financing with tax planning objectives.

- Update: Under the 2026 Act 60 reforms, new applicants are subject to a 4% fixed tax on capital gains and passive income, replacing the previous 0% rate. However, the program has been extended through 2055, providing long-term stability for investors.

Puerto Rico Luxury Properties for Sale

If you’re exploring luxury properties for sale in Puerto Rico, financing becomes far easier when your search is guided by a local luxury team that understands lender expectations, due diligence timing, and what can delay closing. At Christie’s International Real Estate Puerto Rico, we connect qualified buyers to the right inventory and trusted local resources—so you can move from pre-approval to contract with clarity and confidence as you review the sample listings below.

500 PLANTATION DR #PH-3403 DORADO PR, 00646

Exclusive two-level penthouse at Plantation Village in Dorado Beach offering over 12,000 sq. ft. of furnished luxury living, expansive terraces, six bedrooms, resort views, premium amenities, and access to the Ritz-Carlton Reserve lifestyle.

30 FLAMBOYAN GREENS HUMACAO PR, 00791

This fully remodeled corner townhouse in Flamboyan Greens at Palmas del Mar offers golf views, added privacy, modern renovations, a private pool, gazebo, terrace, and access to resort amenities.

13 PEDROSA ST. GARDEN HILLS GUAYNABO PR, 00966

This luxury Garden Hills estate on a rare double lot features 3+ bedrooms, terraces, an infinity pool, koi ponds, a wine cellar, an elevator, and prime gated living near San Juan.

Calle Taft COND. PLAYA GRANDE #9F, SAN JUAN, PR 00911

Bright 1,526 sq. ft. three-bedroom residence at Cond. Playa Grande offers sweeping Atlantic, Condado, and El Yunque views, direct beach access, resort-style amenities, and the opportunity to create your ideal coastal home.

Conclusion

Financing luxury homes in Puerto Rico requires navigating a unique landscape of local lenders, extended timelines, and specialized requirements that differ significantly from mainland markets. Success depends on understanding these constraints early in the process and working with experienced professionals who know the local market dynamics. While the challenges are real, proper preparation and realistic expectations enable buyers to secure financing for their dream properties in this Caribbean paradise.

At Christie's International Real Estate Puerto Rico, we guide our clients through every aspect of luxury home acquisitions, including connecting them with appropriate financing resources and managing the extended closing process. Our deep local knowledge and global network ensure that financing complexities don't derail your luxury property investment in Puerto Rico's most exclusive markets.