With Puerto Rico's booming real estate market, the value of luxury properties has been steadily appreciating, offering exceptional returns on investment. Christie's International Real Estate Puerto Rico offers premier listings of luxury properties for sale, providing high-net-worth individuals with exclusive access to homes that align with the island's tax advantages and long-term investment opportunities.

Avoiding double taxation in Puerto Rico real estate investments now depends on strict, documented compliance with Act 60 and Act 22 rules that have grown sharper and less forgiving. Recent legislative and regulatory updates effective by 2026 increase scrutiny on how Act 60 donations and report filings are documented and verified.

In this article, we outline how serious investors should structure their Puerto Rico real estate strategies around these changes to protect their tax position from day one.

Key Takeaways

Double taxation risk increases when Act 60 compliance is poorly documented.

Bona fide Puerto Rico residency requires more than meeting the 183-day rule.

Pre-move gains can remain taxable by the IRS after relocation.

Act 60 donation and filing requirements must be completed every year.

Puerto Rico luxury real estate can support both residency planning and long-term investment goals.

How Double Taxation Risks Have Changed for Puerto Rico Real Estate Investors

Act 38's 2026 updates layer additional requirements on top of the existing Act 60 framework, tightening the definition of qualifying activity and adding reporting obligations that demand more from decree holders annually.

What the IRS Is Actually Looking For

The IRS does not simply count days. Auditors examine the full picture of where your life is anchored, and they use three tests to make that determination.

Physical presence test: Most investors rely on spending at least 183 days per year in Puerto Rico to satisfy the physical presence test, though the IRS regulations also recognize other, more complex day‑count formulas.

Tax home test: Your primary place of business or employment must be in Puerto Rico, not in a U.S. state.

Closer-connection test: Your social, family, and economic ties must point to Puerto Rico more than to any U.S. state. This includes where your bank accounts are held, where your family lives, where you vote, and where your principal residence is.

Failing any one of these tests in a given year breaks your bona fide residency status for that year and potentially exposes all Puerto Rico-sourced income from that year to U.S. federal tax.

Pre-Move Built-In Gains: A Frequently Missed Trap

One of the most common double-taxation triggers for Puerto Rico real estate investors is the treatment of pre-move built-in gains. If you owned appreciated U.S. assets before relocating to Puerto Rico, the IRS taxes the portion of any gain that accrued before your move date, regardless of where you live when you sell.

Gains that accrued before your Puerto Rico residency start date remain U.S.-taxable even after you establish bona fide residency.

Gains that accrue after your residency start date, on assets that qualify as Puerto Rico-sourced, receive the Act 60 exemption.

Proper documentation of asset values at the date of your move is not optional. It is the baseline that separates exempt gains from taxable ones.

An investor who moved to Puerto Rico in 2021 and sold a property in 2024 without establishing the pre-move cost basis faces a full IRS audit risk on the entire gain, not just the post-move portion.

Updated Charity Donation Thresholds and Act 60 Compliance

Act 38's 2026 updates are expected to raise scrutiny on how these donations are documented and verified, which means informal giving or poorly receipted contributions may not count toward the threshold.

How to Structure Donations for Compliance

Identify Puerto Rico-registered nonprofits that qualify under Act 60 guidelines before the end of each calendar year.

Confirm that at least $5,000 of your annual giving goes to organizations with a documented anti-child-poverty mission.

Request official receipts that include the organization's Puerto Rico tax ID, the date of the donation, and the amount.

Keep copies of all receipts with your annual Act 60 compliance filing.

Do not wait until December. Spreading donations across the year reduces the risk of missing the threshold due to administrative delays.

A Scenario Where This Goes Wrong

Consider an investor who made $8,500 in qualifying donations in year two of their decree, intending to make up the shortfall in January of the following year. That shortfall triggers a compliance gap for the prior year. The $10,000 requirement is annual, not cumulative, and a gap year can give the IRS grounds to challenge the decree's validity for that period.

Investors holding Puerto Rico luxury real estate as their primary asset need to treat the donation requirement with the same discipline they apply to their property tax filings.

The Two-Year Property Purchase Window and Principal Residence Rule

Act 60 requires decree holders to purchase a principal residence in Puerto Rico within two years of receiving their decree. This is not a soft guideline. Missing the window without a documented and approved extension can jeopardize the decree itself, which means losing the tax exemptions the decree was designed to provide.

The principal residence rule also plays a direct role in satisfying the closer-connection test, which makes the property purchase both a legal requirement and a strategic residency anchor.

What Qualifies as a Principal Residence

The property must be your primary home in Puerto Rico, not a vacation property or investment unit.

You must actually live there for the majority of your time in Puerto Rico, not simply own it.

Renting the property out for extended periods while you stay elsewhere in Puerto Rico can weaken your closer-connection argument.

The property must be titled in your name or in a structure that the Puerto Rico Department of Economic Development and Commerce recognizes as compliant.

Strategic Timing Within the Two-Year Window

Waiting until month 23 to close on a property creates unnecessary risk. Title searches, financing delays, and permitting issues in Puerto Rico can push a closing past the deadline. Serious investors begin their property search within the first six months of receiving their decree.

Puerto Rico luxury homes in Dorado, Condado, and Old San Juan are among the most sought-after options for decree holders because they combine principal residence functionality with long-term appreciation potential. Dorado Beach residences, for example, offer both the lifestyle ties that support the closer-connection test and the asset quality that sophisticated investors expect from Puerto Rico luxury real estate.

Now that the property and donation requirements are clear, the more complex coordination challenge involves how U.S. federal and Puerto Rico tax rules interact when income crosses between the two systems.

Coordinating U.S. Federal and Puerto Rico Tax Rules to Prevent Double Taxation

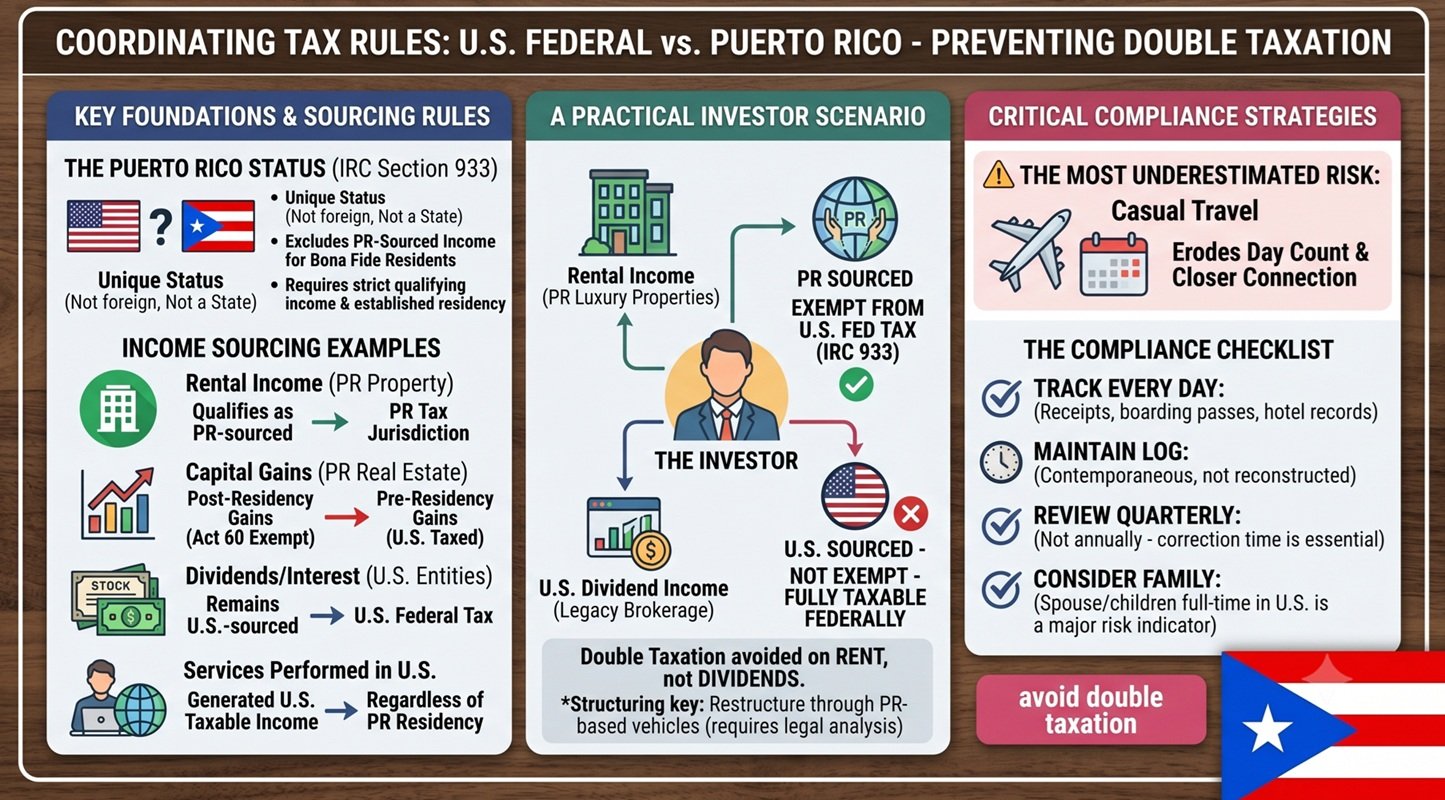

Puerto Rico sits in a unique position within the U.S. tax system. It is not a foreign country, but it is not a U.S. state either. That creates a specific set of rules under IRC Section 933 that exclude Puerto Rico-sourced income from U.S. federal tax for bona fide residents, but only when the income truly qualifies as Puerto Rico-sourced and only when residency is fully established.

The coordination challenge is that many investors hold income streams that cross between U.S.-sourced and Puerto Rico-sourced categories, and the IRS applies strict sourcing rules to determine which side of the line each dollar falls on.

Income Sourcing Rules That Affect Puerto Rico Real Estate Investors

Rental income from Puerto Rico property: Generally qualifies as Puerto Rico-sourced and falls under Puerto Rico tax jurisdiction for bona fide residents.

Capital gains on Puerto Rico real estate: Post-residency gains on Puerto Rico property qualify for the Act 60 exemption. Pre-residency gains do not.

Dividends and interest from U.S. entities: These remain U.S.-sourced and subject to U.S. federal tax even if you are a bona fide Puerto Rico resident.

Income from services performed in the U.S.: Days worked in U.S. states generate U.S.-sourced income taxable at the federal level, regardless of your Puerto Rico residency.

A Practical Investor Scenario

An investor holds a portfolio of Puerto Rico luxury properties generating rental income, plus U.S. dividend income from a legacy brokerage account. The rental income from Puerto Rico real estate qualifies as Puerto Rico-sourced and is exempt from U.S. federal tax under IRC Section 933 as long as bona fide residency holds. The dividend income from the U.S. brokerage account does not qualify for the exemption and remains fully taxable at the federal level.

That investor avoids double taxation on the rental income but not on the dividends. The structuring decision here is whether to restructure the brokerage account through Puerto Rico-based vehicles that generate Puerto Rico-sourced income instead, which requires careful legal and tax analysis before any move.

Day Count Discipline and the Closer-Connection Test in Practice

Perhaps the most underestimated compliance risk is casual travel. Investors who spend extended time in New York, Miami, or other U.S. cities for business or family reasons can unknowingly erode their 183-day count and weaken their closer-connection argument at the same time.

Track every travel day with dated receipts, boarding passes, and hotel records.

Maintain a contemporaneous log, not a reconstructed one. Reconstructed logs carry less weight in an audit.

Review your day count quarterly, not annually. Catching a shortfall in September gives you time to correct it. Catching it in January does not.

Consider where your immediate family lives. A spouse and children remaining full-time in a U.S. state is one of the strongest indicators the IRS uses to challenge closer connection.

With the compliance landscape now mapped out, the most useful thing to leave you with is a structured checklist that reflects the current enforcement environment rather than the more relaxed standards of earlier years.

Investor Compliance Checklist for the Current Enforcement Environment

The IRS Act 60 compliance campaign is not winding down. If anything, the combination of Act 38's 2026 updates and increased agency resources means that decree holders face more scrutiny going forward, not less. Aligning your behavior with the current enforcement environment requires treating each of the following items as a standing obligation, not a one-time task.

Annual Compliance Actions

Count and document every day spent in Puerto Rico versus U.S. states and foreign countries.

Confirm your tax home remains in Puerto Rico through active business filings and employment records.

Complete and file your annual Act 60 report and pay the required annual fee before the deadline.

Make all charitable donations totaling at least $10,000, with at least $5,000 directed to anti-child-poverty organizations, and collect official receipts (at least $5,000 must go to organizations on the government‑approved list dedicated to eradicating child poverty).

Review your income sources to confirm which qualify as Puerto Rico-sourced and which remain U.S.-taxable.

Retain copies of utility bills, bank statements, and other records that demonstrate active Puerto Rico residency.

Structural Actions for New Decree Holders

Begin your principal residence search within the first six months of receiving your decree, not the last six months of your two-year window.

Document the fair market value of all appreciated assets as of your move date to establish the pre-move baseline for capital gains sourcing.

Review all existing investment structures with a Puerto Rico tax attorney to identify U.S.-sourced income streams that may need restructuring.

Avoid holding Puerto Rico luxury real estate in U.S. entities that could complicate the sourcing analysis for rental income and capital gains.

Establish Puerto Rico-based banking, professional, and social ties that collectively support the closer-connection test.

Investors who treat these items as active, documented practices rather than background assumptions are the ones who survive IRS scrutiny with their decrees and exemptions intact.

Luxury Properties and Houses for Sale in Puerto Rico

9 CASTAÑA ST GUAYNABO PR, 00968

9 Castaña St. is a 10,000+ square-foot, seven-bedroom multigenerational estate in San Patricio featuring resort-style outdoor amenities, a private gym, backup utilities, and convenient access to Condado and Dorado.

206 LEGACY DORADO PR, 00646

This Legacy estate in Dorado Beach offers 16,746 sq. ft. of luxury living with bespoke amenities, expansive grounds, and refined indoor-outdoor spaces for privacy, elegance, and modern resort-style living.

32 SHELL CASTLE HUMACAO PR, 00791

32 Shell Castle is a refined oceanfront Palmas del Mar residence offering sweeping Atlantic views, modern indoor-outdoor living, resort-style amenities, solar power, and access to one of Puerto Rico’s premier coastal communities.

413 SOLAR C BO. PUNTAS, RINCÓN, PR 00677

Casa Sol in Puntas, Rincón is a striking brutalist coastal retreat with modern sustainable features, an infinity pool, partial ocean views, and walkable access to Sandy Beach.

Conclusion

Avoiding double taxation in Puerto Rico real estate requires careful planning, clean documentation, and full compliance with Act 60 rules. Investors should treat residency, charitable donations, income sourcing, and the two-year property purchase window as ongoing obligations, not one-time steps. With the right legal, tax, and real estate guidance, Puerto Rico can remain a strong destination for tax-efficient luxury property investment.

Looking to buy, sell, or rent luxury property in Puerto Rico? Christie's International Real Estate Puerto Rico helps investors and high-net-worth residents navigate premium real estate opportunities with trusted local expertise. Connect with our team today to explore luxury properties in Puerto Rico that align with your lifestyle, investment, and relocation goals.

FAQs

How can I avoid estate tax in Puerto Rico?

Puerto Rico does not have an estate tax, making it an appealing option for U.S. investors looking to minimize estate taxes on their Puerto Rican assets. For U.S. citizens, the estate tax only applies federally to non-Puerto Rican assets. To maximize Puerto Rico's estate tax benefits, investors should focus on Puerto Rican-sourced income and assets, ensuring compliance with Act 60's residency requirements to avoid overlapping tax obligations.

Is there a double tax treaty for Puerto Rico?

As a territory in the U.S., Puerto Rico does not have a separate double tax treaty from the United States. However, U.S. citizens and residents can benefit from tax exemptions under Section 933, which excludes Puerto Rican-sourced income from U.S. federal income tax if they meet bona fide residency requirements. This exemption minimizes the risk of double taxation, especially for U.S. investors who qualify as Puerto Rican residents under Act 60.

Can I move to Puerto Rico to avoid capital gains tax?

Yes, U.S. investors can move to Puerto Rico to benefit from capital gains tax exemptions on Puerto Rican-sourced gains if they meet bona fide residency requirements under Act 60. By establishing residency in Puerto Rico and meeting the 183-day physical presence rule, investors may qualify for capital gains exemptions, significantly reducing their tax burden compared to U.S. mainland rates, which can be up to 20% on capital gains. However, capital gains on assets acquired before establishing residency may still be subject to U.S. tax.

Do I need Puerto Rico wills, entity updates, or insurance changes after moving under Act 60?

Often yes. Updating estate documents, ownership structures, and property/umbrella coverage to Puerto Rico residency can prevent probate delays, title issues, and mismatched tax reporting—especially if you hold real estate through LLCs or trusts.

What records should I keep to defend my “principal residence” beyond the deed?

Maintain a clear living footprint: utility bills in your name, PR driver’s license, voter registration, HOA correspondence, local medical/providers, school records (if applicable), and evidence your household goods and primary vehicles are based in Puerto Rico.

How should I handle property management and short-term rentals without weakening residency optics?

Use written leases, a Puerto Rico-based property manager, and consistent local operations (permits, lodging taxes, PR bank accounts). Avoid patterns that make your “home” look like a full-time rental while you primarily live elsewhere.

Does Puerto Rico offer a homestead exemption for primary residences?

Yes, Puerto Rico provides a homestead exemption for primary residences, which protects part of a property’s value from creditors and lowers certain tax liabilities.