Property owners in Puerto Rico must report all rental income to Hacienda, the island's treasury department, regardless of property type or rental duration. Reporting requirements vary significantly between short-term rentals (STRs) and long-term rentals (LTRs). Each category faces different tax rates, deductions, and compliance obligations.

Understanding these distinctions helps property owners avoid costly penalties and maximize their investment returns.

Key Takeaways

- Property owners must file Form 482 annually to report all rental income to Hacienda regardless of the amount or property type.

- Short-term rentals mandate tourist licenses and tax collection while long-term units usually just need municipal permits.

- Meticulous digital record-keeping of expenses is the best defense against Hacienda audits and compliance errors.

- Strategic deduction of maintenance costs and capital depreciation can significantly reduce your overall tax liability.

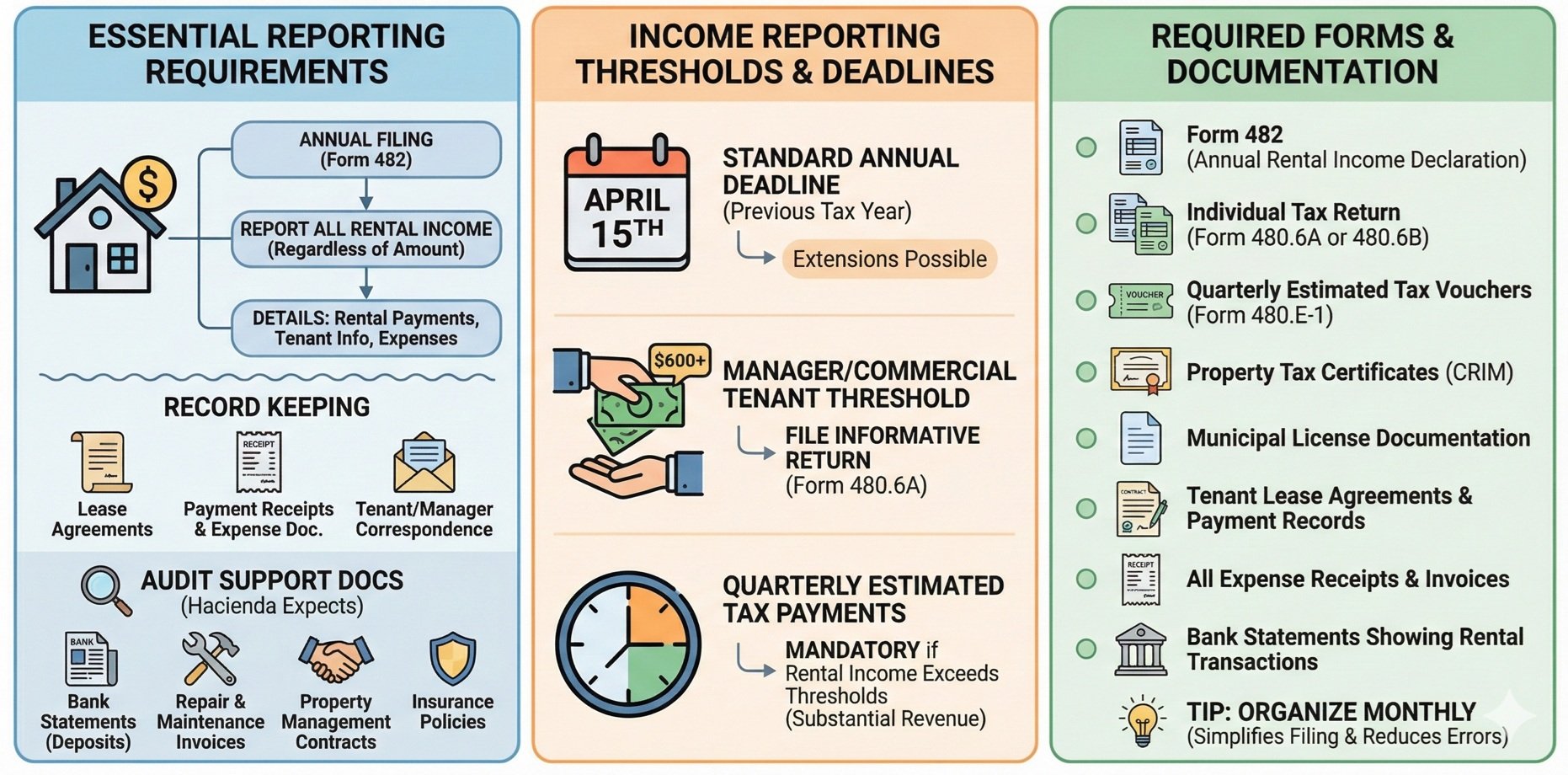

Essential Reporting Requirements for All Rental Properties

Puerto Rico property owners must file their Individual Income Tax Return (Form 482) annually, regardless of rental income amount. This form details all rental payments received, tenant information, and property expenses throughout the tax year.

-

You also need to maintain complete records including lease agreements, payment receipts, expense documentation, and any correspondence with tenants or property managers.

The required documentation includes bank statements showing rental deposits, invoices for repairs and maintenance, property management contracts, and insurance policies. Hacienda expects these documents to support all income and deduction claims during potential audits.

Income Reporting Thresholds and Deadlines

Property owners must report all rental income on their individual tax returns, regardless of the total amount earned.

- The $600 threshold applies specifically to property managers or commercial tenants, who are required to file an Informative Return (Form 480.6A) for payments made to the owner above this amount.

- The standard filing deadline falls on April 15th for the previous tax year, though extensions may be available under specific circumstances.

Quarterly estimated tax payments become mandatory when rental income exceeds certain thresholds, particularly for properties generating substantial monthly revenue.

Required Forms and Documentation

- Form 482 (Annual Rental Income Declaration)

- Individual tax return (Form 480.6A or 480.6B)

- Quarterly estimated tax vouchers (Form 480.E-1)

- Property tax certificates (CRIM)

- Municipal license documentation

- Tenant lease agreements and payment records

- All expense receipts and invoices

- Bank statements showing rental transactions

Organizing these documents monthly rather than waiting until tax season simplifies the filing process and reduces compliance errors.

Short-Term Rental Tax Treatment and Compliance

Short-term rentals in Puerto Rico face more complex tax obligations than traditional long-term leases. Property owners must obtain a tourist accommodation license from the Puerto Rico Tourism Company before accepting guests, and this license requires annual renewal with associated fees. The income from STRs gets taxed at ordinary income rates, which range from 0% to 33% depending on total annual income.

STR operators must collect and remit a 7% accommodation tax from guests, plus applicable municipal taxes that vary by location. This creates additional administrative responsibilities beyond standard income tax reporting.

Licensing and Registration Requirements

The tourist accommodation license application requires property inspections, safety certifications, and compliance with local zoning regulations. Municipal permits may also be necessary, particularly in areas like Old San Juan and Condado where short-term rental regulations are more restrictive.

Properties must display license numbers in all marketing materials and booking platforms like Airbnb, and violations can result in significant fines or license revocation.

Quarterly Tax Obligations

- File quarterly returns by the 20th of April, July, October, and January

- Remit 7% accommodation tax collected from guests

- Pay estimated income taxes on rental profits

- Submit guest occupancy reports to tourism authorities

- Maintain detailed booking and payment records

Long-Term Rental Income Strategies

Long-term rental properties benefit from more straightforward tax treatment and fewer administrative requirements than short-term rentals. Property owners typically need only basic rental licenses from local municipalities, and the income reporting follows standard real estate investment guidelines. LTR income also qualifies for more generous deduction opportunities, including depreciation schedules that can significantly reduce taxable income.

The tax advantages become more pronounced for properties held longer than one year, as they qualify for favorable capital gains treatment upon sale.

Deductible Expenses for Long-Term Rentals

- Mortgage interest payments

- Property management fees (typically 8-12% of gross rental income)

- Routine maintenance and repairs

- Property insurance premiums

- Municipal and state property taxes

- Utilities paid by the owner

- Professional services (legal, accounting, real estate)

- Advertising and marketing costs

- Travel expenses for property management

Depreciation Benefits

Residential rental properties can be depreciated over 27.5 years using the straight-line method, providing annual deductions that often offset significant portions of rental income. This depreciation continues regardless of actual property value appreciation, creating tax shelter opportunities for successful rental investments.

Commercial properties follow a 39-year depreciation schedule, while certain improvements may qualify for accelerated depreciation under specific circumstances.

Rental Tax and Licensing Requirements by Property Type

Understanding these distinctions helps property owners choose the most tax-efficient rental strategy for their specific situation and investment goals.

|

Rental Type |

Tax Rate |

Required Licenses |

Reporting Frequency |

Guest Taxes |

|---|---|---|---|---|

|

Short-Term (STR) |

0-33% ordinary income |

Tourism accommodation license |

Quarterly |

7% accommodation tax |

|

Long-Term (LTR) |

0-33% ordinary income |

Basic municipal rental license |

Annual |

None |

|

Vacation Rental |

0-33% ordinary income |

Tourism + municipal licenses |

Quarterly |

7% + municipal taxes |

|

Corporate Rental |

18.5% corporate rate |

Business license required |

Annual |

Varies by agreement |

Maximizing Deductions and Tax Benefits

Puerto Rico property owners can significantly reduce their tax burden through strategic expense planning and proper documentation. The key lies in understanding which expenses qualify for immediate deductions and which require capitalization and depreciation over time. Professional property management, routine maintenance, and operational costs generally qualify for immediate deduction, while major improvements and renovations must be depreciated.

Property owners frequently miss substantial deduction opportunities simply by failing to track and document eligible expenses throughout the year.

Immediate vs. Capital Improvements

Repairs that maintain the property's current condition qualify as immediate deductions, while improvements that add value or extend useful life must be capitalized. Replacing a broken air conditioning unit represents a deductible repair, but installing central air conditioning in a property that previously lacked it constitutes a capital improvement.

The distinction significantly affects cash flow, as immediate deductions reduce current-year taxes while capital improvements provide benefits over many years through depreciation.

Professional Service Deductions

- Property management company fees

- Real estate attorney consultations

- Accounting and tax preparation services

- Property inspection and appraisal costs

- Insurance agent commissions

- Cleaning and maintenance services

- Landscaping and pool maintenance

Avoiding Common Compliance Mistakes

Property owners frequently face penalties for preventable errors in rental income reporting and tax compliance. The most common mistakes involve inadequate record-keeping, missed filing deadlines, and incorrect classification of expenses or rental types. Hacienda has increased enforcement activities in recent years, particularly targeting short-term rental operators who fail to properly collect accommodation taxes.

Simple organizational systems prevent most compliance issues and significantly reduce audit risk.

Critical Mistake Prevention Checklist

- License Verification: Confirm all required licenses remain current and properly displayed

- Tax Collection: Collect and remit all applicable guest taxes for short-term rentals

- Income Reporting: Report all rental income, including cash payments and barter arrangements

- Expense Documentation: Maintain receipts and invoices for all claimed deductions

- Filing Deadlines: Mark quarterly and annual filing dates on calendar systems

- Bank Account Separation: Use dedicated accounts for rental income and expenses

- Professional Guidance: Consult tax professionals for complex situations or significant income levels

- Municipal Compliance: Stay current with local rental regulations and permit requirements

- Guest Registration: Maintain accurate guest records for tourism reporting requirements

- Insurance Coverage: Ensure adequate coverage for rental activities and liability exposure

Record-Keeping Best Practices

Digital record-keeping systems provide the most reliable approach to tax compliance, allowing easy retrieval during audits and simplified annual filing preparation. Cloud-based accounting software can automatically categorize expenses and generate required reports for Hacienda submissions.

Physical backup copies of critical documents should be maintained separately from digital files to ensure continuity during system failures or data corruption events.

Working with Tax Professionals and Hacienda

Complex rental income situations benefit significantly from professional tax guidance, particularly when properties generate substantial income or involve multiple rental types. Qualified Puerto Rico tax professionals understand local regulations, recent law changes, and audit procedures that general practitioners might miss. The investment in professional services often pays for itself through optimized deduction strategies and penalty avoidance.

Hacienda audits have become more sophisticated and frequent, making professional representation valuable for property owners with significant rental activities.

When to Seek Professional Help

Property owners should consider professional assistance when rental income exceeds $50,000 annually. You should also seek help if operating both rental types simultaneously or facing a Hacienda audit. Complex ownership structures, such as partnerships or LLCs, also warrant professional guidance due to additional reporting requirements.

Recent changes to Puerto Rico tax incentive programs affect some rental property owners, particularly those with Act 60 benefits or other special tax status.

Audit Preparation and Response

- Organize all requested documents promptly and completely

- Provide only information specifically requested by auditors

- Maintain professional communication throughout the process

- Consider professional representation for complex cases

- Document all interactions and correspondence with Hacienda

- Understand appeal rights and procedures if disagreements arise

Luxury Properties and Houses for Sale in Puerto Rico

Luxury properties and houses for sale in Puerto Rico offer unique rental income opportunities, thanks to the island's high demand from both tourists and seasonal residents. Christie's International Real Estate Puerto Rico provides a distinguished selection of premium properties that cater to investors seeking profitable rental ventures in this vibrant market.

152 SAN JUSTO ST SAN JUAN PR, 00901

This 10-unit residential building in Old San Juan blends colonial character with modern functionality, offering 10,800 square feet of prime investment potential in one of Puerto Rico’s most sought-after historic districts.

50 SAN FRANCISCO ST SAN JUAN PR, 00901

This beautifully renovated 2,716 SF Spanish Colonial home in Old San Juan, next to the Governor's Mansion, features historic tilework, soaring 20-foot ceilings, original archways, modern amenities, balconies with picturesque views, and a prime location near top landmarks and dining.

1 - 2 HARBOUR VIEW DRIVE #1 - 2 HUMACAO PR, 00791

This grand three-level oceanview estate offers timeless elegance, expansive living and entertaining spaces, four bedrooms, resort-style outdoor amenities, and a private landscaped setting with panoramic coastal views.

5R MOUNT RESACA BARRIO FLAMENCO CULEBRA PR, 00775

Hilltop Vacation Rental Homes is a five-building, income-producing hospitality property on Mount Resaca in Culebra offering panoramic island and Caribbean views, strong rental history, resort-style amenities, solar and water infrastructure, and easy access to beaches, town, the airport, and ferry.

Conclusion

Successful rental income reporting in Puerto Rico requires understanding the distinct requirements for different property types, maintaining meticulous records, and staying current with evolving tax regulations. Property owners who establish proper systems early avoid most compliance issues and maximize their investment returns through strategic tax planning.

At Christie's International Real Estate Puerto Rico, we're here to guide you in buying, selling, or renting luxury properties in Puerto Rico. Our team's real estate agents and realtors have expertise that ensures seamless transactions, maximizes your investment potential, and caters to your unique real estate goals. Connect with us today!

FAQs

How do I report income from Puerto Rico?

You must file a local tax return with the Puerto Rico Department of Treasury to report income from Puerto Rico, especially rental income. Ensure you accurately report all income sources and claim eligible deductions, such as maintenance, repairs, and management fees. Reporting requirements may vary slightly for properties that qualify for Act 60 incentives, so consult a local tax expert to ensure compliance with Puerto Rican tax laws.

Is rental income taxable in Puerto Rico?

Yes, rental income earned from properties in Puerto Rico is subject to local taxation. Tax rates may vary depending on your residency status and the property's location. Puerto Rico also allows deductions for certain expenses, which can reduce taxable rental income. Additionally, investors who qualify under Act 60 may benefit from significantly reduced or even exempt rental income tax rates, provided they meet residency and other specific requirements.

What qualifies as Puerto Rico source income?

Puerto Rico source income includes income earned within the island, such as rental income from properties in Puerto Rico. Any income generated through local activities or property rentals is considered Puerto Rico source income and is subject to Puerto Rican tax laws rather than U.S. federal tax. However, U.S. citizens may have additional reporting requirements for IRS purposes.

Is any income earned in Puerto Rico exempt from U.S. taxes?

Yes, Puerto Rico is exempt from certain U.S. tax requirements, meaning that local income is primarily subject to Puerto Rico’s tax system.

Do I need to file both Puerto Rico and U.S. tax returns if I am a resident of Puerto Rico?

Generally, U.S. citizens who become residents of Puerto Rico only need to report their income derived from sources within Puerto Rico on their local tax return, unless they have additional U.S.-sourced income.

Do I need to report rental income if I’m a nonresident or only rent the property occasionally?

Yes. Puerto Rico–source rental income is generally reportable to Hacienda even if you live off-island or rent only part of the year; your filing method and any withholding rules can vary based on residency and how the property is held.

What happens if a booking platform collects the accommodation tax—am I still responsible?

Often yes. Even when a platform remits taxes, owners typically must ensure the property is properly licensed/registered and keep proof of amounts collected and remitted, since liability can still fall on the operator if records are incomplete or filings are missed.

How should I handle mixed use (personal use plus rentals) for deductions?

Track rental days vs. personal-use days and allocate shared expenses (e.g., utilities, insurance, repairs) accordingly; only the rental portion is generally deductible, and good logs help support the allocation if questioned.